Executive Summary

The global Information Technology (IT) services industry stands at the beginning of its most significant transformation since the commercialization of the Internet. For more than three decades, companies such as Tata Consultancy Services (TCS), Infosys, Wipro, HCLTech, Cognizant, Accenture, Capgemini, IBM Consulting and several other technology leaders successfully built trillion-dollar market capitalization opportunities by industrializing software engineering through standardized delivery models, global talent pools, process excellence, and operational efficiency. Their success was founded on the ability to develop, integrate, maintain and modernize enterprise applications at an unprecedented scale.

Artificial Intelligence (AI), however, represents a fundamentally different business paradigm. Unlike previous technology waves such as enterprise applications, cloud computing or digital transformation, AI does not merely improve software; it transforms how enterprises create knowledge, automate decisions, generate intellectual property and build competitive advantage. Consequently, the traditional IT services business model, which has historically depended on workforce expansion and project-based revenues, is facing structural disruption.

Most large IT companies have responded by investing heavily in workforce reskilling, Generative AI certifications and AI-enabled service offerings. While these initiatives are strategically essential, they are unlikely to be sufficient on their own to satisfy the speed of technological evolution or the growth expectations of investors. AI innovation increasingly depends on proprietary models, research capabilities, specialized engineering talent, unique datasets, AI platforms and software products rather than on engineering scale alone.

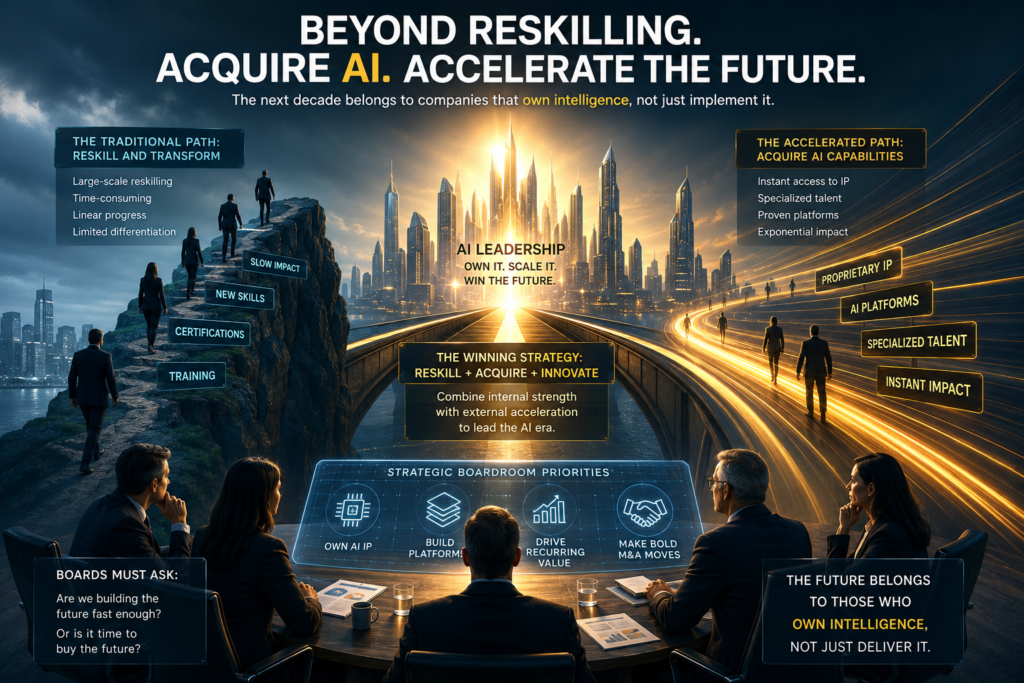

This article argues that the next generation of technology leaders will be distinguished not simply by the number of AI-certified engineers they employ but by their ability to combine internal capability development with strategic mergers and acquisitions (M&A), acqui-hiring, AI product development, platform ownership and ecosystem partnerships. The objective is not to replace workforce transformation but to accelerate it through the acquisition of AI-native companies that already possess the intellectual property, engineering capabilities and innovation culture required for success in the intelligence economy.

The transition from software delivery to intelligence delivery represents more than a technological evolution. It represents a complete redefinition of enterprise value creation and corporate growth.

The Golden Era of Traditional IT Services

Few industries have transformed the global economy as profoundly as the Information Technology services sector. Beginning in the early 1990s, the rapid adoption of enterprise computing, globalization and internet connectivity enabled the emergence of a new business model that fundamentally reshaped how organizations consumed technology. Rather than developing every application internally, enterprises increasingly outsourced software development, maintenance, testing and infrastructure management to specialized technology partners capable of delivering high-quality services at scale.

India emerged as the global leader of this transformation. Companies including TCS, Infosys, Wipro, HCLTech, Tech Mahindra and Cognizant established delivery centers that combined engineering excellence with process maturity, standardized methodologies and cost competitiveness. These organizations successfully demonstrated that software development could be managed as an industrial process supported by globally distributed teams, rigorous quality systems and repeatable execution models.

Over the following three decades, the industry continuously expanded its service portfolio. Enterprise Resource Planning (ERP) implementation, Customer Relationship Management (CRM), Business Intelligence (BI), application modernization, cloud migration, cybersecurity, infrastructure management, digital engineering and consulting services became integral components of the global IT outsourcing ecosystem.

This model generated substantial value for clients and shareholders alike. Enterprises benefited from lower operating costs, faster technology deployment and access to specialized technical expertise, while IT service providers achieved remarkable revenue growth, expanding global footprints and consistently improving shareholder returns.

The success of this industry was built upon five enduring strategic pillars.

| Traditional IT Success Factor | Business Impact |

|---|---|

| Global Engineering Workforce | Large-scale project execution |

| Standardized Delivery Processes | Predictable quality and efficiency |

| Offshore Delivery Model | Cost competitiveness |

| Enterprise Application Expertise | Long-term customer relationships |

| Operational Excellence | Sustainable profitability |

These strategic capabilities enabled traditional IT companies to become trusted technology partners for thousands of enterprises across manufacturing, banking, healthcare, retail, telecommunications, government and financial services.

However, every successful business model eventually encounters technological disruption.

Mainframe computing gave way to client-server architecture. Client-server computing evolved into web applications. Enterprise software expanded into cloud computing. Digital transformation reshaped customer engagement. Each technological revolution required organizations to reinvent themselves while leveraging existing strengths.

Artificial Intelligence represents another such inflection point. Unlike previous transitions, however, AI challenges not merely the technologies organizations use but the very foundations of how value is created, how engineering talent is deployed and how competitive advantage is sustained.

The capabilities that made traditional IT companies exceptionally successful during the software era remain valuable. Nevertheless, they are increasingly becoming necessary conditions for competition rather than sufficient sources of differentiation.

Artificial Intelligence Is Not Another Technology Cycle

Many organizations continue to treat Artificial Intelligence as another incremental technology upgrade similar to cloud migration, mobile application development or robotic process automation. Such comparisons significantly underestimate the transformational nature of AI.

Cloud computing changed where software runs.

Digital transformation changed how organizations operate.

Artificial Intelligence changes how organizations think.

This distinction explains why AI is disrupting virtually every function within the enterprise simultaneously. Unlike previous technology investments that primarily improved operational efficiency, AI directly influences knowledge creation, strategic decision-making, customer interactions, product development, research, engineering, finance, legal operations, marketing, supply chain management and executive leadership.

For the first time in modern business history, organizations are deploying systems capable of generating new content, reasoning across multiple knowledge domains, interpreting complex documents, identifying patterns within enormous datasets and supporting decision-making that historically depended almost exclusively on human expertise.

Consequently, enterprises are beginning to compete not merely on operational excellence but on the quality of their organizational intelligence.

This transformation fundamentally changes the economics of technology investment.

Historically, technology investments generated returns by reducing costs, improving efficiency or increasing operational productivity. AI investments increasingly generate returns by creating entirely new products, accelerating innovation, improving strategic decisions, enhancing customer experiences and enabling autonomous business operations.

The result is a significant shift in enterprise priorities.

| Previous Technology Waves | AI Transformation Era |

|---|---|

| Process Automation | Cognitive Automation |

| Cost Reduction | Revenue Expansion |

| Software Deployment | Intelligence Creation |

| Operational Efficiency | Strategic Decision Support |

| Human Productivity | Human–AI Collaboration |

| Digital Transformation | Business Model Transformation |

This evolution also changes what investors value.

Capital markets have historically rewarded IT services companies for predictable execution, steady revenue growth, operational discipline and strong cash flows. These characteristics remain important, but they no longer represent the only drivers of enterprise valuation.

Today’s investors increasingly seek evidence that organizations possess differentiated AI capabilities capable of generating sustainable long-term growth. They evaluate companies based on their ability to build proprietary intellectual property, launch AI-enabled products, develop scalable platforms and establish defensible competitive advantages that cannot easily be replicated.

Consequently, market expectations have shifted beyond operational excellence toward innovation excellence.

This change presents both an extraordinary opportunity and a significant strategic challenge for traditional IT companies.

Their existing strengths in software engineering, client relationships, global delivery and enterprise transformation provide an excellent foundation for AI adoption. However, these capabilities alone may not enable them to compete against organizations whose business models, engineering cultures and investment strategies were designed around Artificial Intelligence from inception.

The emergence of AI-native companies demonstrates this new reality. These organizations are typically built around proprietary algorithms, specialized research teams, AI-first architectures and product-centric business models. Rather than selling engineering effort, they increasingly commercialize intelligence itself.

This distinction has profound implications for the future of the global IT services industry.

The competitive landscape is gradually shifting from organizations that excel at building software toward organizations that excel at building intelligence. Companies that recognize this transition early will have the opportunity to redefine their business models, diversify revenue streams and create new sources of enterprise value. Those that continue to view AI merely as another technology service may discover that they are competing in a market whose rules have fundamentally changed.

Artificial Intelligence is therefore not simply another chapter in the evolution of enterprise technology. It represents the beginning of a new economic era in which intellectual property, AI platforms, proprietary models and organizational intelligence become the primary drivers of corporate growth and long-term competitive advantage.

The Structural Difference Between Software Engineering and AI Engineering

The widespread belief that Artificial Intelligence is simply another extension of software engineering is one of the biggest strategic misconceptions shaping boardroom discussions today. This assumption has encouraged many organizations to conclude that reskilling existing software engineers alone will be sufficient to compete in the AI economy. While software engineering remains the foundation upon which AI applications are built, AI engineering represents a distinct multidisciplinary discipline that combines computer science with statistics, mathematics, data science, cognitive science, machine learning, distributed computing and domain expertise.

Traditional software engineering is primarily concerned with designing deterministic systems. Engineers define business rules, translate functional requirements into algorithms, write code, test functionality and deploy applications whose outputs remain predictable for a given input. Success depends upon software quality, scalability, reliability, maintainability and operational performance.

AI engineering operates under an entirely different paradigm. Instead of explicitly programming every business rule, AI engineers build systems capable of learning patterns from data, adapting to changing environments, generating new content, making probabilistic predictions and continuously improving through feedback. The engineer is no longer programming every decision. The engineer is designing an intelligence system that learns how to make decisions.

This distinction fundamentally changes the skills required to build enterprise solutions.

| Traditional Software Engineering | AI Engineering |

|---|---|

| Rule-based programming | Data-driven learning |

| Deterministic outputs | Probabilistic outputs |

| Software architecture | Intelligence architecture |

| Application development | Model development and orchestration |

| Debugging code | Evaluating models and reasoning |

| Structured databases | Structured and unstructured data |

| Business logic | Statistical inference |

| System deployment | Continuous model optimization |

This shift also transforms the educational foundation of engineering. Many successful software professionals spend decades building enterprise applications without applying advanced mathematics beyond fundamental programming concepts. AI engineering requires engineers to understand probability theory, statistics, optimization, linear algebra, embeddings, vector representations, model evaluation, uncertainty estimation and increasingly the principles governing large language models and autonomous agents.

Programming therefore remains necessary, but it is no longer sufficient.

Another important distinction concerns the nature of enterprise assets. Traditional software organizations primarily create value by developing applications. AI organizations increasingly create value by developing proprietary intelligence. Data pipelines, vector databases, foundation models, retrieval systems, reasoning architectures and AI agents become strategic assets comparable to patents or proprietary manufacturing processes. Competitive differentiation shifts from writing better software to building better knowledge systems.

This evolution explains why enterprises implementing AI initiatives often discover that their greatest challenge is not software development but data quality, governance, domain expertise, experimentation and organizational readiness.

The New Economics of Engineering Talent

The emergence of AI has also changed the economics of engineering talent.

For decades, the competitive strength of traditional IT companies was closely correlated with workforce scale. Revenue growth generally required hiring additional engineers, expanding delivery centres and increasing project capacity. This created a highly successful linear business model in which organizational growth was directly linked to engineering headcount.

Artificial Intelligence disrupts this relationship.

An AI platform developed by a relatively small engineering team may generate enterprise value comparable to that created by thousands of software developers working on traditional projects. A proprietary AI product can be licensed globally without proportionately increasing engineering resources. Autonomous agents can automate knowledge-intensive work that previously required large project teams.

Consequently, intellectual property increasingly becomes more valuable than workforce size.

| Previous IT Economy | AI Economy |

|---|---|

| Workforce Scale | Intellectual Property |

| Delivery Capacity | AI Capability |

| Project Expansion | Platform Expansion |

| Human Effort | Autonomous Intelligence |

| Service Contracts | Software Products |

| Time-Based Billing | Subscription and Usage Revenue |

| Resource Utilization | AI Adoption and Customer Value |

This transformation challenges one of the historical assumptions underlying the global IT services industry: that sustainable growth depends primarily upon expanding engineering capacity.

In the AI economy, sustainable growth increasingly depends upon expanding proprietary capability.

Organizations capable of building reusable AI platforms, industry-specific models, enterprise copilots and autonomous business applications may achieve significantly higher operating leverage than organizations dependent exclusively on project-based services.

This is one reason why investors increasingly differentiate between technology companies that primarily provide engineering services and those that own scalable AI products and platforms.

Why Reskilling Alone Will Not Create AI Leaders

The response of most large IT companies to the AI revolution has been both logical and necessary. Massive investments have been made in workforce reskilling, AI certifications, internal learning platforms, Generative AI boot camps and partnerships with technology vendors.

These initiatives represent an essential first step.

However, they should not be mistaken for a complete transformation strategy.

The challenge lies in the speed at which AI evolves. Large language models, reasoning models, multimodal AI, autonomous agents, synthetic data generation, AI observability, model optimization and orchestration frameworks are advancing at a pace rarely witnessed in enterprise technology. New capabilities emerge within months, while enterprise reskilling programmes often require years to achieve organization-wide adoption.

This creates an inevitable innovation gap.

Large organizations must standardize training, establish governance, redesign processes and manage organizational risk before deploying new technologies at scale. AI-native startups operate under very different conditions. They experiment rapidly, release products continuously and refine solutions based on immediate market feedback.

The difference is structural rather than cultural.

Traditional IT companies optimize for reliability.

AI-native companies optimize for discovery.

Traditional IT organizations emphasize process maturity.

AI startups emphasize experimentation.

Traditional delivery organizations minimize uncertainty.

AI organizations deliberately embrace uncertainty because experimentation is often the pathway to innovation.

These differences do not suggest that one operating model is superior to the other. They simply demonstrate that organizations optimized for software delivery are not automatically optimized for AI innovation.

This explains why internal reskilling, although indispensable, may not generate AI leadership by itself.

Leadership in AI increasingly depends upon access to specialized researchers, proprietary models, domain-specific datasets, advanced AI infrastructure, product management capability and an organizational culture designed around continuous experimentation.

These capabilities require far more than training programmes.

They require organizational transformation.

Why AI-Native Companies Possess Structural Advantages

Perhaps the most significant strategic development in the technology industry is the emergence of AI-native companies.

Unlike traditional software businesses that later incorporated AI capabilities, AI-native companies were designed around Artificial Intelligence from inception. Their architecture, products, engineering practices, customer propositions and organizational cultures assume AI as the central operating principle rather than an additional feature.

This creates several structural advantages.

First, AI-native companies typically build proprietary intellectual property instead of customized client solutions. Every engineering investment contributes to a reusable platform rather than a single implementation project.

Second, these companies attract highly specialized talent whose expertise extends beyond software development into machine learning research, reinforcement learning, model evaluation, data engineering, computational linguistics, robotics, distributed computing and AI safety.

Third, their product development cycles are considerably shorter because organizational structures encourage experimentation instead of extensive delivery governance.

Finally, AI-native companies frequently operate platform-based revenue models that generate recurring subscription income and improve operating leverage as customer adoption expands.

| Traditional IT Firm | AI-Native Company |

|---|---|

| Client Projects | AI Products |

| Delivery Excellence | Product Innovation |

| Customized Solutions | Scalable Platforms |

| Workforce Expansion | Intellectual Property Expansion |

| Process Optimization | Continuous Experimentation |

| Service Revenue | Recurring Platform Revenue |

| Operational Efficiency | Knowledge and Intelligence Assets |

These structural characteristics explain why relatively small AI companies can sometimes influence entire industries despite employing only a fraction of the workforce of traditional technology firms.

Their competitive advantage lies not in organizational size but in technological differentiation.

This reality presents an important strategic implication for traditional IT companies.

Attempting to recreate every AI capability internally may prove slower, more expensive and strategically riskier than selectively acquiring organizations that already possess differentiated technology, specialized engineering talent and commercially validated AI products.

This observation does not diminish the importance of internal capability development. Rather, it highlights that the future of enterprise AI will likely be determined by how effectively organizations combine internal transformation with external capability acquisition.

The companies that successfully integrate experienced enterprise engineering teams with AI-native innovation cultures will be significantly better positioned to compete than organizations pursuing either strategy in isolation.

The next decade will therefore not be defined by a competition between traditional IT companies and AI startups. It will be defined by how effectively traditional technology leaders evolve into AI-first enterprises capable of combining operational excellence with continuous innovation.

That transformation requires more than learning new technologies.

It requires rethinking the very architecture of corporate growth.

The M&A Imperative: Why Buying AI Capabilities May Be Faster Than Building Them

Every major technological disruption has produced a common strategic dilemma for established market leaders. Should new capabilities be developed internally, or should they be acquired from organizations that have already demonstrated technological leadership?

History consistently suggests that successful companies rarely depend exclusively on one approach. Instead, they combine internal capability development with carefully selected acquisitions that accelerate innovation, shorten time-to-market and reduce strategic uncertainty.

Artificial Intelligence is likely to reinforce this pattern.

The speed of AI innovation has become unprecedented. New foundation models, reasoning architectures, autonomous agents, multimodal systems and domain-specific AI applications are emerging within months rather than years. Building every capability internally requires significant investment, extended research cycles and sustained organizational commitment. By the time many organizations complete internal development, the market may have already shifted toward the next generation of AI technologies.

Strategic acquisitions offer an alternative path.

Rather than purchasing revenue alone, organizations can acquire capabilities that would otherwise require years to develop. These include experienced AI researchers, specialized engineering teams, proprietary algorithms, enterprise AI platforms, industry-specific products, valuable datasets, established customer relationships and innovation cultures that have already demonstrated commercial success.

The objective of AI-focused mergers and acquisitions should therefore extend far beyond increasing company size.

It should accelerate organizational intelligence.

| Traditional Acquisition Objective | AI-Era Acquisition Objective |

|---|---|

| Market Expansion | Capability Expansion |

| Revenue Growth | Intellectual Property Growth |

| Customer Acquisition | AI Platform Acquisition |

| Geographic Presence | Specialized AI Talent |

| Service Portfolio Expansion | Product and Model Innovation |

| Operational Synergies | Innovation Acceleration |

This distinction changes the way boards should evaluate acquisition opportunities. Future transactions should increasingly be assessed according to the strategic capabilities they introduce rather than purely the financial metrics they contribute.

Buying Time Instead of Building Slowly

Perhaps the greatest competitive advantage of AI acquisitions is speed.

Technology companies have traditionally enjoyed the luxury of multi-year transformation programmes. Artificial Intelligence offers no such comfort.

Competitive advantage now evolves continuously.

Every major model release introduces new capabilities.

Every advancement in reasoning, inference optimization, synthetic data generation or autonomous agents raises customer expectations.

Every new AI startup increases competitive pressure.

Organizations relying exclusively on internal transformation may discover that their capability development cycles remain significantly slower than the pace of technological innovation.

Strategic acquisitions effectively purchase time.

Instead of spending several years recruiting researchers, assembling engineering teams, developing products, validating market demand and establishing technical credibility, organizations can acquire companies that have already completed these stages of development.

In rapidly evolving technology markets, reducing time-to-market often creates greater strategic value than reducing acquisition cost.

Time itself becomes a competitive asset.

Why Capital Markets Reward AI Differently

The expectations of financial markets have also changed.

Historically, investors rewarded IT services companies for predictable earnings growth, disciplined execution, expanding customer relationships and operational efficiency. Stable cash flows, healthy utilization levels and recurring enterprise contracts created confidence in long-term business performance.

Artificial Intelligence introduces new valuation drivers.

Investors increasingly examine whether organizations possess proprietary AI capabilities capable of generating sustainable competitive advantage beyond traditional service delivery.

Questions raised by institutional investors are gradually changing.

Does the company own proprietary AI platforms?

Can its AI products generate recurring subscription revenue?

Does it possess differentiated intellectual property?

Can it commercialize AI globally?

Does it have access to scarce AI talent?

Can AI significantly improve operating leverage?

Can AI create entirely new revenue streams rather than simply improving existing services?

These questions influence future valuation because they relate directly to long-term growth potential rather than short-term operational performance.

This explains why AI announcements increasingly influence market sentiment even before meaningful financial returns become visible.

Markets value future capability.

Not merely present performance.

The AI Valuation Equation

The traditional IT services industry has historically operated according to a relatively linear growth equation.

Additional customers required additional engineers.

Additional projects required additional delivery centres.

Revenue expansion generally required workforce expansion.

Artificial Intelligence introduces operating leverage that challenges this relationship.

A single AI platform can simultaneously serve thousands of enterprise customers.

An autonomous AI agent can perform work previously requiring large delivery teams.

An enterprise copilot can improve productivity across multiple industries without proportionate increases in engineering resources.

A domain-specific AI platform can generate recurring subscription revenue independent of workforce growth.

The relationship between revenue and employee count therefore begins to weaken.

| Traditional Growth Model | AI Growth Model |

|---|---|

| More Employees | More AI Platforms |

| More Projects | More Products |

| More Delivery Teams | More Autonomous Systems |

| Higher Utilization | Higher Intelligence |

| Linear Revenue Growth | Scalable Recurring Revenue |

| Services | Products + Platforms + Services |

This evolution explains why investors increasingly differentiate between technology companies that own AI assets and organizations that primarily provide engineering capacity.

Ownership of intelligence increasingly commands higher strategic value than ownership of labour capacity.

Why AI-Native Acquisitions Can Create Long-Term Competitive Advantage

The acquisition of AI-native companies should not be viewed simply as a mechanism for purchasing technology.

Its greatest value often lies in acquiring organizational capability.

Technology can eventually be replicated.

Culture is considerably more difficult to reproduce.

Many AI-native organizations operate with research-oriented cultures that encourage experimentation, rapid prototyping, interdisciplinary collaboration and continuous innovation. Engineers, researchers, product managers and domain experts frequently work together within highly integrated teams.

Such organizational behaviour is difficult to establish through traditional corporate restructuring alone.

Strategic acquisitions therefore introduce more than software.

They introduce new ways of thinking.

When effectively integrated, acquired AI companies can influence engineering practices, accelerate product innovation, improve research capability and transform organizational culture across the acquiring enterprise.

The most successful acquisitions are therefore not absorbed into existing structures.

They gradually reshape those structures.

Lessons from Global Technology Leaders

The world’s leading technology companies rarely rely upon a single innovation strategy.

They invest heavily in internal research while simultaneously acquiring emerging technologies, forming strategic partnerships, funding startup ecosystems and recruiting specialized talent.

This balanced approach reflects a recognition that innovation originates from multiple sources.

Internal engineering teams provide scale, enterprise relationships and operational excellence.

Startups contribute speed, experimentation and breakthrough innovation.

Academic institutions generate foundational research.

Venture capital ecosystems identify emerging technologies before they become mainstream.

Successful corporations increasingly position themselves at the centre of this innovation network rather than attempting to generate every capability internally.

This principle is becoming equally relevant for traditional IT services organizations.

Future leadership will depend less upon building the largest engineering workforce and more upon building the strongest innovation ecosystem.

The AI Growth Flywheel

The AI economy rewards organizations capable of creating self-reinforcing cycles of innovation.

One strategic model for traditional IT companies is the AI Growth Flywheel.

| Strategic Driver | Enterprise Outcome |

|---|---|

| AI-Native Acquisitions | Specialized Talent and Intellectual Property |

| Proprietary AI Platforms | Differentiated Products |

| Product Innovation | Higher Customer Value |

| Customer Adoption | Recurring Revenue |

| Recurring Revenue | Increased Investment Capacity |

| Increased Investment | Further AI Innovation and Acquisitions |

Unlike traditional service businesses where growth primarily depends upon increasing delivery capacity, the AI Growth Flywheel compounds competitive advantage over time.

Every successful product generates additional investment.

Every acquisition strengthens intellectual property.

Every innovation expands customer adoption.

Every new customer generates additional data, insights and product improvement opportunities.

Growth therefore becomes increasingly self-reinforcing.

The AI M&A Decision Matrix

Not every AI acquisition creates strategic value.

Boards should therefore evaluate potential acquisitions using capability-based criteria rather than purely financial metrics.

| Evaluation Dimension | Strategic Question |

|---|---|

| Intellectual Property | Does the company own differentiated AI technology? |

| Engineering Talent | Does the acquisition strengthen AI capability? |

| Product Maturity | Has the technology demonstrated commercial adoption? |

| Platform Potential | Can the technology scale across industries? |

| Data Advantage | Does the company possess unique datasets or domain expertise? |

| Cultural Compatibility | Can innovation culture be preserved after integration? |

| Strategic Alignment | Does the acquisition support long-term corporate strategy? |

This framework shifts acquisition discussions away from traditional financial analysis toward long-term strategic capability building.

From Workforce Expansion to Intelligence Expansion

The global IT services industry was built through workforce expansion.

The AI economy will increasingly be built through intelligence expansion.

This does not diminish the importance of engineers.

On the contrary, software engineering will remain the foundation of enterprise technology.

However, future engineering organizations will increasingly be measured by the quality of their AI platforms, proprietary models, innovation ecosystems and intellectual property rather than solely by the number of professionals they employ.

The strategic objective for traditional IT companies should therefore not be choosing between reskilling and acquisitions.

The objective should be accelerating enterprise transformation through the intelligent combination of both.

Organizations that rely exclusively on internal reskilling risk moving more slowly than technological change.

Organizations that rely exclusively on acquisitions risk creating fragmented portfolios lacking organizational integration.

The future belongs to companies capable of integrating experienced enterprise engineering teams with AI-native innovation, product thinking and strategic capital allocation.

Artificial Intelligence is redefining the architecture of corporate growth.

The next generation of market leaders will not simply deploy AI more effectively.

They will own more of the intelligence economy.

The New Growth Formula for Traditional IT Giants

Artificial Intelligence is forcing the global IT services industry to redefine the drivers of long-term growth. For nearly three decades, success was measured through revenue expansion, client acquisition, delivery excellence, engineering headcount and operational efficiency. These metrics remain important, but they are no longer sufficient to sustain competitive advantage in an economy increasingly shaped by intelligence rather than software alone.

The next generation of technology leaders will require a fundamentally different growth model. Instead of viewing AI as another service offering within an existing portfolio, organizations must recognize AI as the foundation of future business models. This requires a transition from service-centric thinking to platform-centric thinking, from project execution to product innovation, and from workforce expansion to intellectual property creation.

The companies that successfully navigate this transformation are unlikely to abandon their traditional strengths. Their competitive advantage will instead emerge from combining decades of enterprise engineering expertise with AI-native innovation, strategic acquisitions, proprietary platforms and recurring software revenues.

| Legacy Business Model | Future AI Business Model |

|---|---|

| IT Services | AI Solutions and Platforms |

| Project Delivery | Outcome Delivery |

| Customer-Specific Development | Reusable AI Products |

| Engineering Scale | Intelligence Scale |

| Linear Revenue | Recurring Platform Revenue |

| Human Execution | Human-AI Collaboration |

| Operational Excellence | Innovation Excellence |

| Cost Leadership | Knowledge Leadership |

This evolution requires organizations to think beyond technology implementation and begin managing AI as a strategic corporate asset.

What CEOs and Boards Should Do Next

Artificial Intelligence should no longer be viewed as a technology initiative delegated exclusively to engineering teams or information technology departments. It represents a strategic business transformation requiring active involvement from boards of directors, chief executive officers, chief financial officers and corporate strategy leaders.

The first priority should be redefining AI as a long-term corporate growth strategy rather than a short-term productivity initiative. Organizations that evaluate AI solely through cost reduction may overlook its far greater potential to create new products, business models and revenue streams.

The second priority is adopting a balanced capability-building strategy. Internal reskilling should remain a central investment because existing engineering talent possesses deep enterprise knowledge, customer relationships and implementation expertise. However, workforce transformation should be complemented by strategic mergers and acquisitions, acqui-hiring, venture investments, university partnerships and collaborative innovation ecosystems that accelerate access to specialized AI capabilities.

The third priority involves increasing investment in proprietary intellectual property. Sustainable competitive advantage in the AI economy will depend less on implementation capability and more on ownership of reusable AI platforms, domain-specific models, enterprise copilots, autonomous agents and differentiated software products. Intellectual property should become a board-level strategic asset rather than merely an engineering outcome.

The fourth priority is redesigning organizational structures to encourage continuous experimentation. Traditional governance frameworks optimized for predictable project delivery should evolve to support rapid innovation, interdisciplinary collaboration and responsible experimentation while maintaining appropriate controls over security, compliance and AI governance.

Finally, corporate leaders should reassess capital allocation priorities. Future investment decisions should increasingly evaluate whether resources are directed toward building long-term AI capabilities rather than simply expanding short-term delivery capacity. Organizations that consistently invest in proprietary technology, specialized talent and scalable AI platforms are likely to strengthen both their competitive positioning and long-term shareholder value.

The Future Outlook: The IT Services Industry in 2035

By 2035, the distinction between software companies and AI companies is likely to become increasingly blurred. Artificial Intelligence will be deeply embedded across enterprise applications, business processes and customer experiences. However, the most successful organizations will not be those that merely deploy AI tools. They will be those that own the platforms, intellectual property and innovation ecosystems that enable AI at scale.

Traditional IT companies will continue to play a significant role in enterprise transformation because their experience in managing complex technology environments remains invaluable. Nevertheless, their business models are expected to evolve substantially.

Future technology companies are likely to derive a greater proportion of revenue from AI-powered software products, autonomous enterprise platforms, digital engineering ecosystems, subscription-based intelligence services and industry-specific AI solutions. Consulting engagements will increasingly focus on business transformation enabled by AI rather than technology implementation alone.

The boundaries between consulting firms, software companies and AI platform providers will continue to converge. Competitive advantage will depend on an organization’s ability to integrate enterprise knowledge, software engineering, data science, AI research, product innovation and strategic advisory capabilities into a unified value proposition.

Consequently, the defining characteristic of tomorrow’s technology leaders may not be the size of their workforce but the quality of their intellectual property, the strength of their innovation culture and the scalability of their AI platforms.

Conclusion

The global IT services industry stands at a historic turning point.

The same organizations that successfully transformed enterprise computing over the past three decades now face the challenge of transforming themselves. Artificial Intelligence is not simply another technology trend that can be absorbed into existing operating models. It represents a structural shift in how enterprises create value, compete in global markets and generate sustainable growth.

Reskilling existing software engineers is an essential component of this transformation and should remain a strategic priority. It enables organizations to modernize their workforce, strengthen enterprise delivery capabilities and integrate AI into existing customer engagements. However, expecting reskilling alone to create AI leadership may underestimate both the speed of technological disruption and the changing economics of innovation.

At the same time, mergers and acquisitions should not be viewed as a substitute for internal capability development. Acquiring AI-native companies without successfully integrating their technology, talent and culture rarely produces lasting competitive advantage. Sustainable transformation requires organizations to combine enterprise engineering excellence with AI-native innovation through disciplined integration and long-term strategic commitment.

The future therefore does not belong to organizations that choose between reskilling and acquisitions. It belongs to those that successfully orchestrate both. The companies that combine experienced engineering talent, proprietary AI platforms, strategic mergers and acquisitions, research partnerships, product innovation and disciplined capital allocation will be best positioned to lead the next era of enterprise technology.

History has repeatedly shown that every technological revolution rewards organizations willing to reinvent themselves before disruption becomes unavoidable. The AI revolution is unlikely to be different.

The winners of the next technology decade will not simply write better software. They will build better intelligence, create stronger innovation ecosystems and redefine the future of enterprise value creation.

References

- Russell, S., & Norvig, P. (2021). Artificial Intelligence: A Modern Approach (4th ed.). Pearson. https://aima.cs.berkeley.edu/

- Goodfellow, I., Bengio, Y., & Courville, A. (2016). Deep Learning. MIT Press. https://www.deeplearningbook.org/

- Stanford Institute for Human-Centered Artificial Intelligence. (2025). AI Index Report 2025. https://hai.stanford.edu/ai-index

- World Economic Forum. (2025). The Future of Jobs Report 2025. https://www.weforum.org/reports/the-future-of-jobs-report-2025

- McKinsey & Company. (2023). The Economic Potential of Generative AI: The Next Productivity Frontier. https://www.mckinsey.com/capabilities/quantumblack/our-insights/the-economic-potential-of-generative-ai-the-next-productivity-frontier

- PwC. (2024). Global AI Jobs Barometer. https://www.pwc.com/

- Deloitte. (2024). State of Generative AI in the Enterprise. https://www2.deloitte.com/

- Gartner. (2024). Top Strategic Technology Trends. https://www.gartner.com/

- Microsoft. (2024). Work Trend Index Annual Report. https://www.microsoft.com/worklab

- NVIDIA. (2024). State of AI in Enterprise. https://www.nvidia.com/en-us/ai/

- International Data Corporation (IDC). (2024). Worldwide Artificial Intelligence Spending Guide. https://www.idc.com/

- Anthropic. (2025). Research Publications. https://www.anthropic.com/research

- OpenAI. (2025). Research and Developer Documentation. https://platform.openai.com/docs

Disclaimer

The views expressed in this article are the personal strategic opinions of the author and are intended to encourage discussion among business leaders, boards of directors, investors, policymakers and technology professionals. The analysis reflects broad industry trends and should not be interpreted as a definitive assessment of any individual company, its employees or its future performance.

References to organizations such as TCS, Infosys, Wipro, HCLTech, Cognizant, Accenture, IBM Consulting, Capgemini and other technology companies are provided solely for illustrative and analytical purposes because they represent significant participants in the global IT services industry. No conclusions are drawn regarding the current capabilities, strategies or competitive positioning of any specific organization.

The article does not argue that traditional software engineers are incapable of becoming AI engineers. On the contrary, software engineering remains the foundation of modern AI systems. The central argument is that, given the pace of AI innovation and the evolving expectations of capital markets, internal workforce reskilling alone may not be sufficient for every organization to achieve long-term AI leadership. A balanced strategy that combines talent development with product innovation, strategic partnerships, AI-native acquisitions and disciplined integration may enable organizations to accelerate transformation while preserving enterprise strengths.

This article is intended for educational and strategic discussion only and should not be construed as investment advice, financial advice, legal advice or a recommendation to pursue any specific corporate strategy, merger or acquisition. Strategic decisions should always be based on organization-specific analysis, market conditions, regulatory requirements and independent professional advice.