Rethinking Agricultural Mobility, Rural Energy, and Farm Economics in India (2026–2035)

Abstract

The global transition toward sustainable mobility has largely been viewed through the lens of passenger vehicles, commercial transportation, and urban infrastructure. While electric cars, buses, and two-wheelers have dominated policy debates and investment decisions, one of the most consequential opportunities for electrification remains relatively underexplored: agricultural machinery. Among these, the electric tractor has the potential to redefine not only farm mechanization but also rural energy systems, agricultural productivity, equipment economics, and the future business models of agricultural equipment manufacturers.

India presents a uniquely favourable environment for this transformation. Unlike passenger vehicles that depend on an expanding public charging network, tractors operate within predictable geographic boundaries and spend a significant portion of their lifecycle on privately owned agricultural land. Most Indian farmers own or have access to dedicated residential or farm premises where charging infrastructure can be installed with comparatively lower complexity. This characteristic fundamentally changes the economics and operational feasibility of electrification.

The transition to electric tractors, however, should not be viewed as a simple replacement of diesel engines with battery-powered drivetrains. It represents a structural shift from mechanical products to intelligent agricultural platforms integrating electrification, software, precision agriculture, artificial intelligence, connected services, renewable energy, and data-driven decision-making. Consequently, future competition in the tractor industry is expected to move beyond horsepower, fuel efficiency, and manufacturing scale toward digital capabilities, ecosystem partnerships, lifecycle services, and farmer productivity.

This article examines the strategic implications of electric tractors for India’s agricultural machinery industry during the period 2026–2035. It analyses market drivers, technology evolution, customer economics, policy considerations, manufacturing transformation, competitive dynamics, and emerging business models. Rather than predicting a rapid replacement of conventional tractors, the paper argues that electrification will occur selectively, beginning with economically attractive applications before expanding into broader market segments. The companies that successfully integrate engineering excellence with software, energy management, and digital agriculture are likely to define the next era of agricultural mechanization.

Introduction

The Four Forces Transforming Agriculture

| Transformation | Traditional Agriculture | Future Agriculture |

| Energy | Diesel | Electricity + Renewable Energy |

| Machinery | Mechanical | Intelligent & Connected |

| Operations | Manual Decisions | AI-Assisted Decisions |

| Business Model | Equipment Sales | Platform Ecosystem |

Every major industrial transformation begins quietly.

The steam engine transformed manufacturing before reshaping global trade. The internal combustion engine redefined transportation long before it became the backbone of industrial economies. The internet began as a communication technology before becoming the operating system of the modern economy. Artificial intelligence, similarly, is evolving from a computational capability into a foundational layer influencing almost every industry.

Agricultural mechanization is approaching a comparable inflection point.

For more than six decades, tractors have remained the single most important mechanical asset on Indian farms. They have improved productivity, reduced dependence on manual labour, accelerated farm operations, and supported India’s transition toward food security. Despite continuous improvements in engine efficiency, hydraulics, transmission systems, ergonomics, and emissions compliance, the fundamental architecture of the tractor has remained largely unchanged. Diesel engines continue to dominate the sector, supported by an extensive ecosystem of manufacturers, suppliers, dealers, service networks, and financing institutions.

Yet the forces reshaping global mobility are beginning to influence agriculture. Climate commitments, energy security concerns, technological advancements, battery cost reductions, artificial intelligence, connected equipment, precision farming, and renewable energy integration are creating conditions that could fundamentally alter how agricultural machinery is designed, manufactured, financed, operated, and serviced.

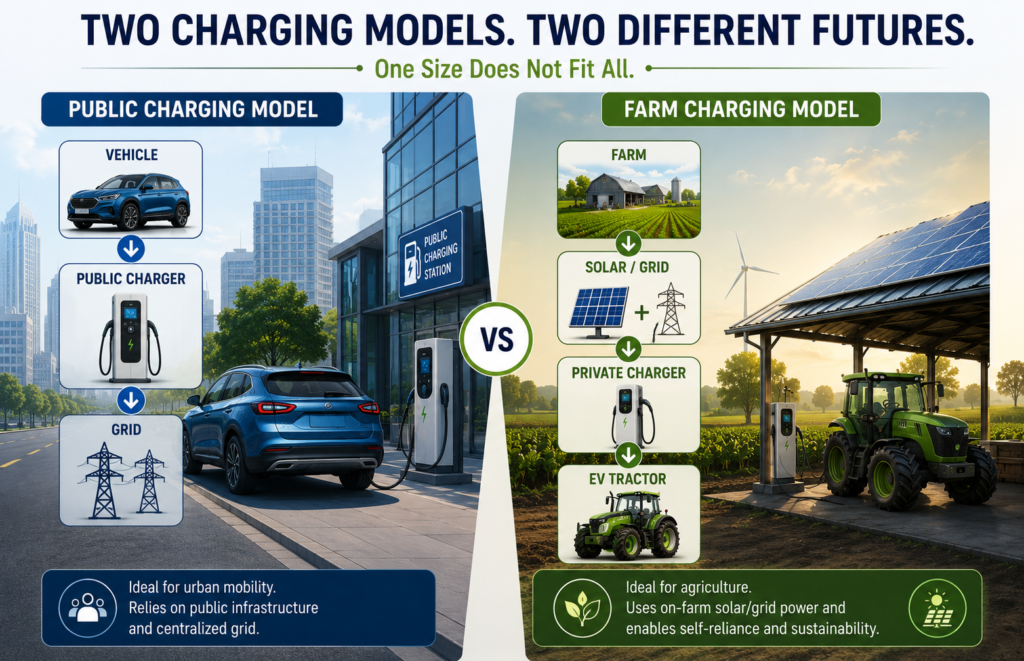

Unlike passenger vehicle electrification, where consumer convenience depends heavily on public charging infrastructure, electric tractors benefit from a fundamentally different operating environment. Most tractors operate within fixed geographic areas, return to the same farm or village after daily operations, and can often be charged overnight on private property. This significantly reduces one of the largest barriers facing urban electric mobility.

India possesses another structural advantage. The country’s agricultural landscape consists largely of owner-operated farms where machinery remains close to the owner’s residence. The availability of private land creates opportunities for installing charging equipment without many of the land acquisition, parking, or public infrastructure challenges associated with urban transportation.

However, the opportunity extends far beyond replacing diesel with electricity.

Electric tractors introduce the possibility of integrating agriculture with distributed renewable energy systems. A tractor could eventually become part of a broader farm energy ecosystem connected to rooftop solar, agricultural solar pumps, on-farm battery storage, and intelligent energy management systems. Such integration has implications not only for operating costs but also for energy resilience and long-term sustainability.

The implications for manufacturers are equally profound.

Historically, competitive advantage in the tractor industry depended primarily on mechanical engineering, manufacturing efficiency, dealer reach, and product reliability. These capabilities will remain essential. However, future differentiation is increasingly likely to emerge from software, electronics, battery management, telematics, artificial intelligence, predictive maintenance, precision agriculture, and integrated digital services.

This evolution changes the basis of competition.

Manufacturers are no longer competing solely to build better tractors. They are competing to build more intelligent agricultural ecosystems capable of improving farm productivity, reducing operating costs, enhancing equipment utilization, and generating recurring revenue through connected services.

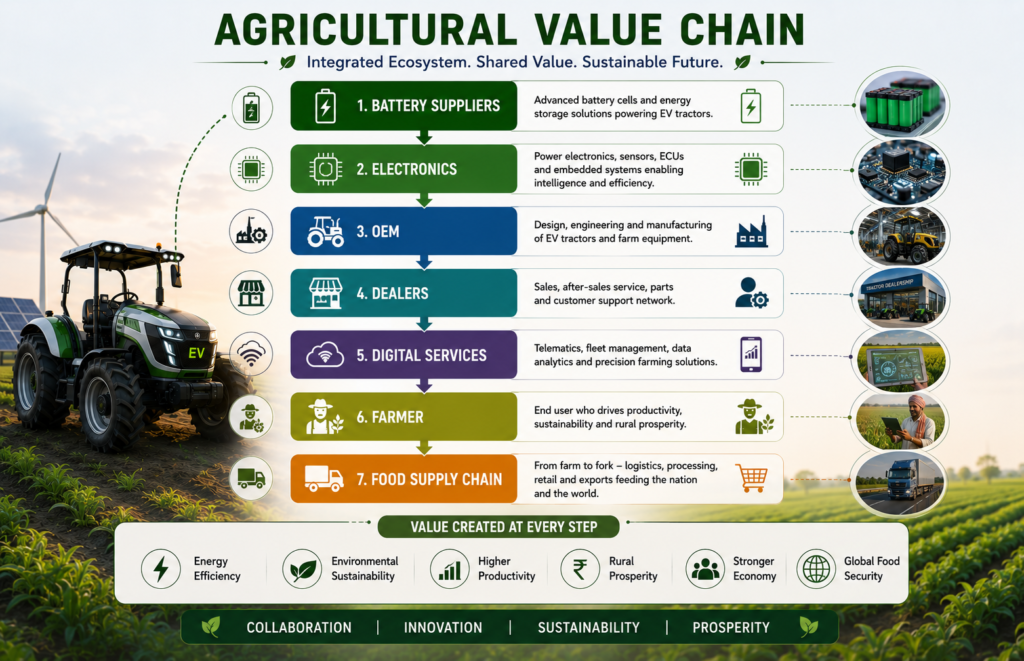

The implications extend beyond original equipment manufacturers. Battery producers, semiconductor companies, software developers, energy providers, financial institutions, agricultural technology startups, telecommunications companies, and renewable energy firms are all becoming participants in the future agricultural value chain. The tractor is evolving from a standalone machine into a connected node within a much larger rural technology ecosystem.

For policymakers, electric tractors represent an opportunity to simultaneously advance agricultural modernization, rural electrification, clean energy adoption, manufacturing competitiveness, and climate objectives. For investors, they create new opportunities across batteries, charging infrastructure, farm software, digital agriculture, and precision equipment. For farmers, the principal question remains straightforward: can electric tractors deliver superior economics without compromising reliability and productivity?

The answer is unlikely to be uniform across all farming applications.

Electrification will probably not replace every diesel tractor during the next decade. High-horsepower applications involving continuous heavy-duty field operations may continue to rely on advanced diesel or alternative technologies for some time. Conversely, compact tractors, orchard operations, horticulture, greenhouse farming, municipal applications, institutional campuses, and light commercial agriculture may emerge as early adoption segments where electric solutions provide measurable economic and operational advantages.

Understanding this transition therefore requires a broader strategic perspective than conventional market forecasts. It demands analysis of customer economics, technology readiness, manufacturing capability, policy frameworks, energy infrastructure, competitive dynamics, financing innovation, and organizational transformation.

The central proposition of this paper is that the future of electric tractors should not be evaluated merely as a product innovation. It should be understood as the convergence of four simultaneous transformations: the electrification of agricultural mobility, the digitization of farming, the decentralization of rural energy systems, and the emergence of agriculture as a data-intensive industry.

Organizations that recognize only the first transformation may successfully manufacture electric tractors. Organizations that understand all four are more likely to shape the future of agricultural mobility itself.

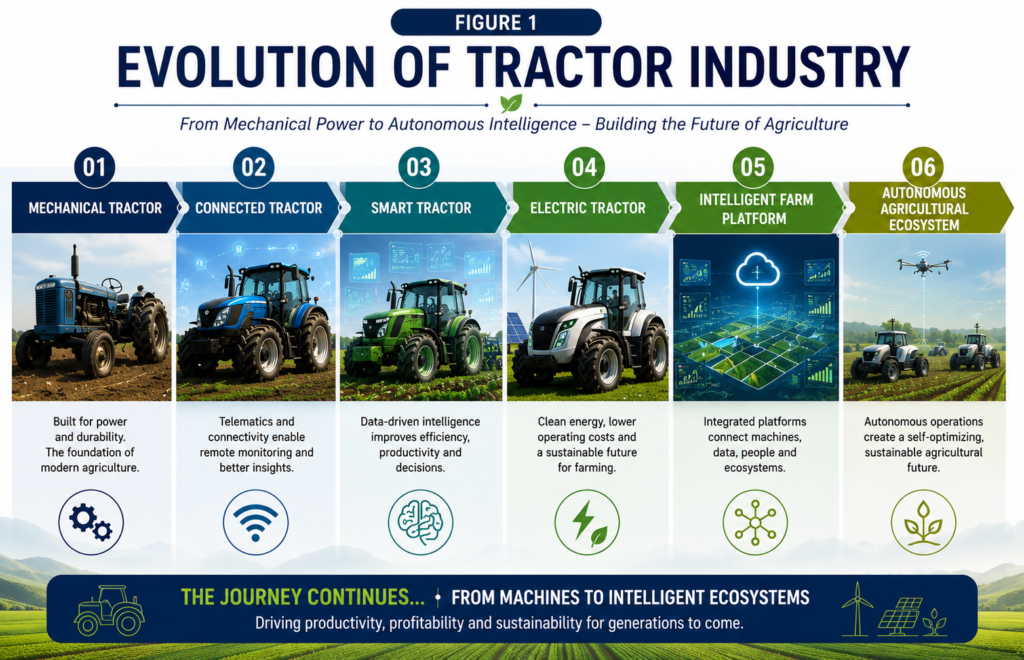

Table 1. Evolution of Agricultural Mechanization

| Era | Primary Driver | Dominant Technology | Source of Competitive Advantage |

| 1960–1985 | Mechanization | Diesel Engine | Mechanical Reliability |

| 1985–2005 | Productivity | Hydraulics & Transmission | Fuel Efficiency |

| 2005–2025 | Precision Farming | GPS, Electronics, Sensors | Product Portfolio & Dealer Network |

| 2026–2035 | Electrification | Battery, AI, Software | Digital Ecosystem & Customer Productivity |

| Beyond 2035 | Intelligent Agriculture | AI, Robotics, Autonomous Systems | Platform-Based Agriculture |

India’s Structural Advantage: Why the EV Tractor Story Will Be Different

Every major technology transition succeeds only when three conditions converge simultaneously: technological feasibility, economic viability, and ecosystem readiness. In many industries, one or more of these conditions develops slowly, delaying large-scale adoption. The electric tractor market in India presents a different strategic picture because several structural characteristics already exist, creating conditions that could support a phased transition over the coming decade.

The first structural advantage is the operating environment. Unlike passenger cars that require extensive public charging infrastructure and frequently travel long distances, tractors generally operate within defined agricultural boundaries. They return to the same village or farm after completing daily activities and often remain idle for extended periods outside seasonal operations. This predictable utilization pattern creates an opportunity for scheduled overnight charging without placing significant pressure on public charging networks.

Table 2. Passenger EV versus EV Tractor

| Parameter | Passenger EV | EV Tractor |

| Charging Location | Public & Home | Primarily Farm/Home |

| Daily Distance | Variable | Predictable |

| Charging Opportunity | Uncertain | Overnight |

| Infrastructure Dependency | High | Moderate |

| Operating Area | National | Localized |

| Fleet Utilization | Medium | Seasonal |

The second advantage is land ownership. A substantial proportion of Indian tractor owners have access to independent residential premises or agricultural land where private charging equipment can potentially be installed. This characteristic fundamentally alters infrastructure economics. Instead of depending on thousands of public charging stations, the initial charging ecosystem for tractors can evolve through decentralized private installations supported by agricultural electricity connections, rooftop solar systems, or dedicated farm energy solutions. The infrastructure challenge therefore becomes significantly more manageable than in urban passenger mobility.

The third advantage lies in utilization economics. Tractor purchasing decisions are generally driven by lifecycle operating costs rather than emotional considerations. Farmers evaluate machinery based on fuel consumption, maintenance expenses, reliability, productivity, financing costs, and resale value. If electric tractors demonstrate a superior total cost of ownership under specific operating conditions, adoption decisions are likely to become increasingly data-driven.

Table 3. Farmer Purchase Decision Framework

| Decision Variable | Diesel Tractor | EV Tractor |

| Purchase Price | Moderate | Higher |

| Fuel Cost | High | Lower |

| Maintenance | Higher | Lower |

| Noise | High | Low |

| Emissions | High | Zero Tailpipe |

| Total Cost of Ownership | Depends on utilization | Depends on utilization and charging economics |

This distinction is strategically important. Passenger vehicle markets often respond to brand image, design, and consumer preferences. Agricultural machinery markets respond primarily to measurable economic outcomes. Consequently, the long-term success of electric tractors will depend less on technological novelty and more on demonstrable improvements in farmer profitability.

Another structural advantage arises from India’s policy environment. National priorities around agricultural modernization, renewable energy expansion, manufacturing competitiveness, digital public infrastructure, and climate commitments increasingly reinforce one another. Although electric tractors may not receive identical policy treatment as passenger electric vehicles, the broader direction of industrial and agricultural policy supports greater mechanization, cleaner technologies, and digital transformation. This alignment creates favourable long-term conditions for innovation without implying that adoption will occur uniformly across all regions or farming segments.

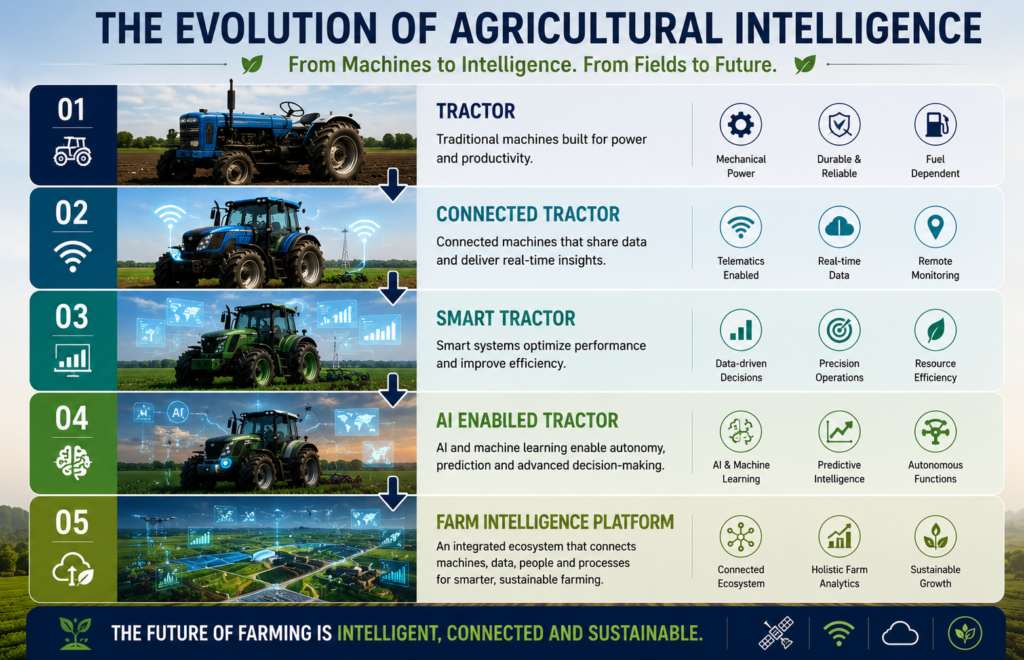

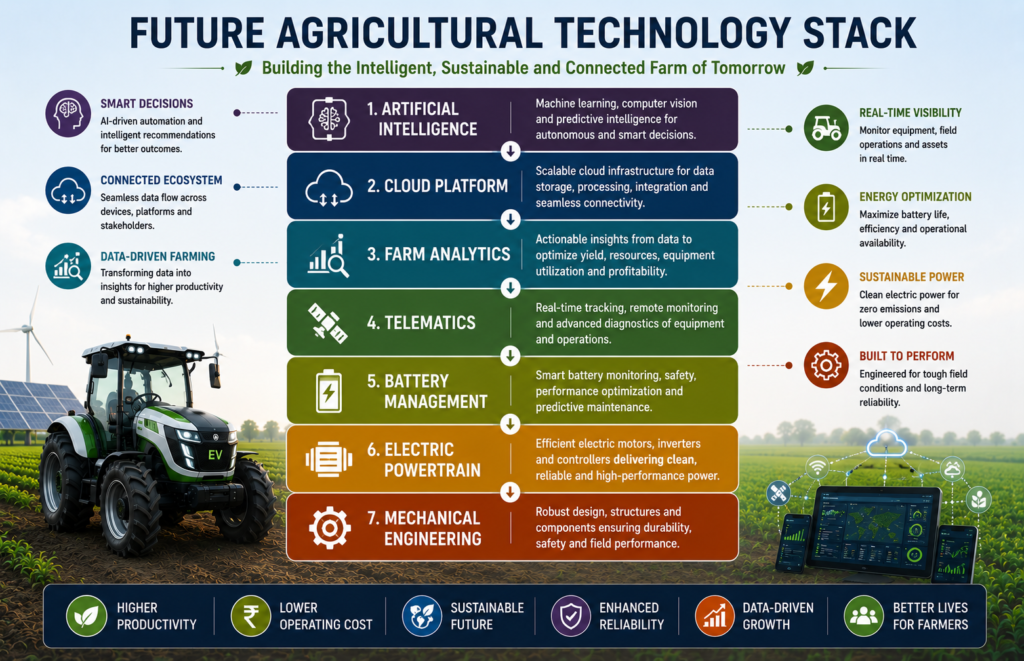

From Mechanical Machines to Intelligent Agricultural Platforms

Perhaps the most significant misconception surrounding electric tractors is that they represent only a powertrain substitution. Such a perspective underestimates the scale of industrial transformation underway.

The conventional tractor has historically been a mechanical asset whose primary purpose was to generate power for agricultural operations. Future agricultural machinery is likely to evolve into intelligent platforms integrating energy management, software, sensors, communications, artificial intelligence, precision farming, and predictive maintenance.

Table 4. Transformation of Tractor Industry

| Traditional OEM | Future Agricultural Technology Company |

| Mechanical Engineering | Mechanical + Electrical + Software |

| Product Sales | Product + Services |

| Spare Parts | Digital Revenue |

| Diesel Engine | Multi-Energy Platforms |

| Dealer | Digital Service Network |

| Tractor | Connected Agricultural Platform |

This transformation mirrors developments already visible in other industries. Modern aircraft generate continuous operational data throughout every flight. Industrial equipment increasingly relies on predictive analytics to optimize maintenance schedules. Manufacturing plants employ digital twins to simulate production systems before implementing operational changes. Agricultural machinery is beginning to follow a similar trajectory.

Electric drivetrains naturally accelerate this transition because they require sophisticated electronic control systems, battery management software, thermal management algorithms, and digital diagnostics. Once digital architecture becomes integral to machine operation, additional services become possible. Remote diagnostics, predictive maintenance, fleet management, agronomic recommendations, energy optimization, and equipment utilization analytics can all be layered onto the physical product.

Consequently, future competitive advantage will not depend solely on manufacturing tractors efficiently. It will increasingly depend on designing integrated platforms capable of continuously creating value throughout the equipment lifecycle.

For manufacturers, this changes the business model itself. Revenue will no longer originate exclusively from machinery sales. Software subscriptions, connected services, equipment monitoring, predictive maintenance, digital agronomy, fleet analytics, financing solutions, and energy services may gradually become additional sources of recurring income. The transition therefore resembles the broader evolution from product-centric industries toward platform-based ecosystems.

The Economics That Will Ultimately Determine Adoption

Table 5. EV Tractor Economics

| Cost Element | Diesel | Electric |

| Fuel | High | Lower (subject to tariff) |

| Engine Maintenance | Higher | Lower |

| Lubricants | Required | Minimal |

| Battery Replacement | Not Applicable | Lifecycle Consideration |

| Electricity | Not Applicable | Required |

| Total Lifecycle Cost | Variable | Application Dependent |

Technological capability alone has never guaranteed commercial success. Farmers invest in machinery because it improves economic outcomes. Therefore, the central question surrounding electric tractors is not whether they can be engineered successfully, but whether they can consistently outperform conventional alternatives on total lifecycle economics.

Several cost categories influence this comparison.

Initial acquisition cost remains one of the most visible barriers. Battery systems continue to represent a significant proportion of electric vehicle manufacturing costs. Although battery prices have declined substantially during the past decade, purchase prices for electric agricultural equipment are still expected to exceed equivalent diesel models in many segments. Financing innovation will therefore become as important as engineering innovation.

Operating expenditure, however, presents a different picture. Electricity generally exhibits lower and more stable operating costs than diesel fuel. Electric drivetrains contain fewer moving components than internal combustion engines, potentially reducing routine maintenance requirements. Elimination of engine oil changes, lower drivetrain complexity, regenerative capabilities in certain operating conditions, and reduced mechanical wear may improve lifecycle economics. Actual savings, however, will depend on utilization patterns, electricity tariffs, charging behaviour, and battery replacement cycles.

Residual value introduces another dimension. Conventional tractors possess well-established secondary markets supported by decades of operating history. Electric tractors must gradually establish similar confidence regarding battery durability, resale values, and long-term serviceability. Transparent battery health assessment, standardized warranties, and certified refurbishment programs may become essential to building confidence within used equipment markets.

Downtime economics may ultimately become even more influential than direct operating costs. Agricultural operations are highly time-sensitive. Delays during sowing or harvesting seasons can significantly affect farm productivity. Manufacturers will therefore need to demonstrate not only lower operating costs but also reliable service networks, rapid diagnostics, spare parts availability, and dependable charging solutions. Reliability remains the foundation upon which all economic arguments rest.

Why Battery Technology Is Only One Part of the Equation

Public discussions frequently reduce electric mobility to battery chemistry. While battery technology is undoubtedly important, long-term competitiveness depends on a much broader engineering system.

Battery management software determines charging efficiency, thermal stability, safety, and lifecycle performance. Power electronics influence energy conversion efficiency. Electric motors affect torque delivery and field performance. Vehicle control software coordinates interactions among propulsion systems, hydraulic functions, operator inputs, and implements. Thermal management becomes increasingly important under India’s diverse climatic conditions.

Consequently, future agricultural machinery manufacturers will increasingly resemble integrated engineering organizations combining expertise in mechanical engineering, electrical engineering, embedded software, data science, artificial intelligence, and systems integration.

This multidisciplinary requirement raises barriers to entry. Traditional strengths in engine manufacturing and mechanical design remain valuable but become only one component of a much larger capability portfolio.

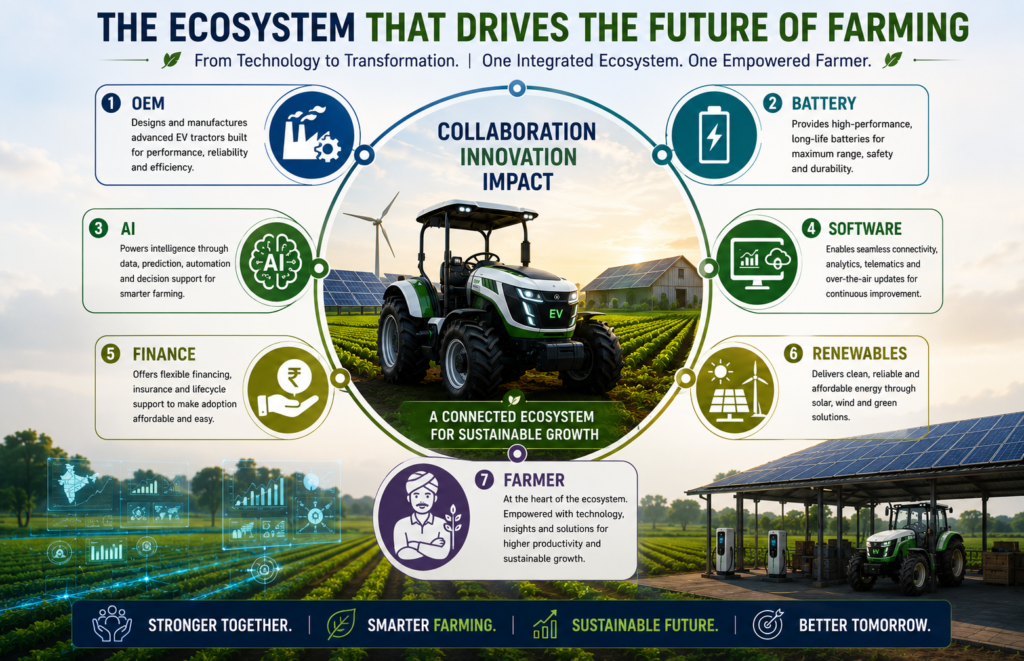

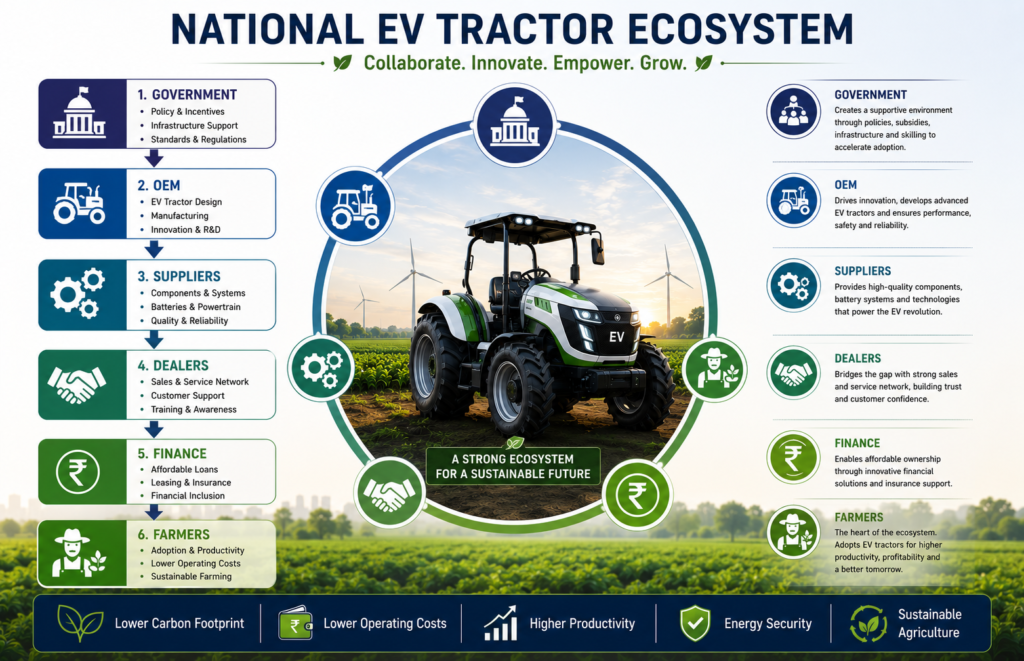

The Emerging Competitive Landscape

Table 6. Future Industry Participants

| Stakeholder | Traditional Role | Future Role |

| OEM | Tractor Manufacturer | Agricultural Platform Provider |

| Battery Company | Supplier | Energy Partner |

| Software Company | Minimal | Core Technology Provider |

| AI Company | None | Precision Agriculture |

| Dealer | Sales & Service | Customer Success Centre |

| Bank | Financing | Mobility-as-a-Service |

The competitive environment surrounding agricultural machinery is expanding beyond conventional tractor manufacturers.

Battery companies are seeking new industrial applications. Semiconductor suppliers are developing automotive-grade electronics suitable for off-highway equipment. Artificial intelligence firms are entering precision agriculture. Telecommunications providers are enabling connected farming solutions. Renewable energy companies view agriculture as a potential distributed energy market. Financial institutions are exploring innovative ownership models. Agricultural technology startups continue introducing specialized software solutions addressing irrigation, crop monitoring, soil analytics, and farm management.

The result is the gradual emergence of an agricultural technology ecosystem rather than a conventional equipment industry.

Original equipment manufacturers therefore face a strategic decision. They can attempt to develop every capability internally, or they can orchestrate partnerships that combine complementary strengths. History suggests that platform leaders often succeed by creating ecosystems rather than attempting complete vertical integration.

This principle becomes particularly relevant in agriculture because farmers rarely purchase isolated technologies. They invest in integrated solutions that improve productivity while minimizing operational complexity. The organizations capable of combining machinery, software, energy, finance, and agronomic intelligence into coherent customer experiences are likely to establish stronger competitive positions than companies focusing exclusively on equipment manufacturing.

The future tractor may therefore become less important as an individual machine and more important as the central operating platform of an increasingly intelligent agricultural enterprise.

Strategic Imperatives for Industry Leaders

Table 7. Strategic Priorities by Stakeholder

| Stakeholder | Strategic Priority |

| OEM | Electrification Strategy |

| Supplier | Electronics Localization |

| Dealer | Digital Capability |

| Government | Charging & Standards |

| Investor | Platform Businesses |

| Farmer | Lifecycle Economics |

The transition toward electric tractors should not be interpreted as an inevitable replacement cycle. Instead, it should be viewed as a strategic option whose pace will vary across customer segments, geographies, applications, and economic conditions. The organizations that succeed will be those that avoid binary thinking. The future is unlikely to belong exclusively to diesel or electric technologies; it is more likely to favour diversified portfolios capable of serving different agricultural use cases while adapting to changing technology and customer preferences.

Board Strategy Matrix

| Time Horizon | Primary Strategic Focus |

| 2026–2028 | Pilot commercialization |

| 2028–2030 | Portfolio expansion |

| 2030–2032 | Connected agriculture |

| 2032–2035 | AI-driven farming ecosystem |

For tractor manufacturers, the most immediate challenge is organizational rather than technological. Most established original equipment manufacturers have spent decades optimizing mechanical engineering, manufacturing efficiency, dealer development, and supply chain management. Those strengths remain valuable and should not be abandoned. However, future competitiveness will increasingly require complementary capabilities in software engineering, embedded electronics, artificial intelligence, battery integration, cybersecurity, cloud platforms, and digital customer engagement. The transition therefore requires expansion rather than replacement of existing competencies.

The evolution of the dealer network will be equally important. Historically, dealers have focused on machinery sales, financing assistance, spare parts, and mechanical service. As connected and electric equipment becomes more prevalent, dealerships may gradually evolve into technology service centres capable of remote diagnostics, software updates, battery health assessment, energy advisory, fleet analytics, and customer education. The dealer relationship may become increasingly continuous rather than episodic, supported by digital engagement throughout the equipment lifecycle.

The supplier ecosystem will also undergo structural change. Traditional suppliers specializing in castings, engines, transmissions, and mechanical components will continue to play critical roles, but demand is expected to expand for batteries, electric motors, inverters, sensors, semiconductors, wiring systems, embedded controllers, and software-enabled electronic components. This transformation creates opportunities for existing suppliers to diversify while encouraging new technology-oriented companies to participate in the agricultural machinery value chain.

Financial institutions should view electrification as an opportunity to redesign agricultural equipment financing. Innovative structures such as battery leasing, equipment subscriptions, residual-value financing, pay-per-use models, and bundled energy solutions could reduce adoption barriers while improving affordability. Such models may become particularly attractive for custom hiring centres, cooperatives, institutional users, and commercial farming enterprises where equipment utilization is relatively high.

The Role of Public Policy

Table 8. Policy Priorities

| Short Term | Medium Term | Long Term |

| Pilot Projects | Charging Ecosystem | Smart Farming |

| Standards | Battery Manufacturing | AI Agriculture |

| Financing | Skill Development | Autonomous Farming |

Public policy has historically influenced the pace of agricultural mechanization through financing support, rural infrastructure, irrigation development, and productivity enhancement initiatives. Future policy discussions surrounding electric tractors should extend beyond purchase incentives.

A more comprehensive policy framework would emphasize research and development, component manufacturing, battery recycling, standards, interoperability, workforce development, rural charging readiness, precision agriculture, digital connectivity, and localized innovation. Such an approach would strengthen the entire agricultural technology ecosystem rather than focusing exclusively on demand stimulation.

Policy coordination across agriculture, heavy industries, renewable energy, power distribution, skill development, and digital infrastructure will become increasingly important. Electrification intersects with multiple sectors, and isolated policy interventions may deliver less value than integrated strategies designed around long-term agricultural productivity and manufacturing competitiveness.

Investors and the Expanding Agricultural Technology Economy

Table 9. Emerging Investment Themes

| Investment Area | Opportunity |

| Battery Manufacturing | Very High |

| Charging Infrastructure | High |

| Precision Agriculture | Very High |

| AI Platforms | Very High |

| Connected Machinery | High |

| Farm Analytics | High |

| Recycling | Medium |

Investment opportunities created by electric tractors extend well beyond vehicle manufacturing.

Investment Opportunity Matrix

| Sector | Growth Potential | Investment Risk | Strategic Importance |

| EV Tractors | High | Medium | Very High |

| Batteries | Very High | Medium | Very High |

| AI Agriculture | Very High | Medium | Very High |

| Charging Infrastructure | High | Medium | High |

| Farm Analytics | High | Low | High |

| Precision Agriculture | Very High | Medium | Very High |

| Battery Recycling | High | Medium | High |

Battery management systems, charging solutions, precision agriculture software, telematics, artificial intelligence, predictive maintenance, agricultural analytics, renewable energy integration, robotics, autonomous technologies, and circular economy solutions all represent emerging areas of commercial interest. Investors should therefore evaluate the agricultural machinery transition as the development of an interconnected technology ecosystem rather than a single-product market.

Private equity firms, venture capital investors, infrastructure funds, and strategic corporate investors may increasingly identify opportunities not only within equipment manufacturing but also across enabling technologies that improve equipment utilization, energy efficiency, and farm productivity.

Looking Toward 2035

Projecting technological transitions requires humility. The history of industrial innovation demonstrates that markets rarely evolve exactly as anticipated. Some technologies mature more rapidly than expected, while others encounter economic, regulatory, or customer adoption constraints. Consequently, strategic planning should be based on scenarios rather than certainty.

A realistic outlook suggests that the Indian tractor market during 2026–2035 will continue to include multiple propulsion technologies. Diesel tractors are expected to remain important, particularly in demanding high-horsepower applications. Electric tractors may progressively establish positions in compact tractors, horticulture, orchards, vineyards, institutional campuses, municipal applications, and selected commercial farming operations where utilization patterns favour electrification. Hybrid approaches and other alternative technologies may also emerge depending on technological progress and market economics.

Irrespective of the pace of electrification, several broader trends appear more durable. Agricultural machinery is expected to become increasingly connected. Artificial intelligence is likely to support operational decision-making across farming and manufacturing. Precision agriculture will continue expanding as data availability improves. Software will become more deeply integrated into machinery. Manufacturers will increasingly compete through ecosystems rather than standalone products. Customer value creation will increasingly depend on productivity improvements achieved throughout the equipment lifecycle rather than at the point of sale alone.

These structural trends suggest that electrification should be understood as one element within a larger transformation of agricultural mobility.

| Timeline | Strategic Focus |

| 2026–2028 | Early Commercialization |

| 2028–2030 | Portfolio Expansion |

| 2030–2032 | Digital Agriculture Integration |

| 2032–2035 | Intelligent Agricultural Ecosystem |

Conclusion

India stands at a strategically important moment in the evolution of agricultural mechanization. The country’s combination of a large tractor market, expanding manufacturing capability, engineering talent, growing digital infrastructure, renewable energy ambitions, and entrepreneurial ecosystem creates favourable conditions for innovation in agricultural equipment.

The opportunity presented by electric tractors is not simply environmental. It is fundamentally economic and strategic. It has the potential to reshape manufacturing, supply chains, software development, rural energy systems, financing models, and customer relationships. Yet its ultimate success will depend not on technological enthusiasm but on demonstrable improvements in farmer productivity, operating economics, reliability, and lifecycle value.

The central question is therefore not whether electric tractors will replace diesel tractors. The more important question is how agricultural machinery companies can evolve from manufacturers of mechanical equipment into providers of intelligent agricultural mobility solutions.

Organizations that continue viewing tractors primarily as machines may remain competitive in the short term. Organizations that recognize tractors as connected technology platforms integrated with energy, software, artificial intelligence, and precision farming are more likely to define the next generation of agricultural leadership.

The future of Indian agriculture may therefore be shaped not merely by electrification, but by the convergence of engineering excellence, digital intelligence, sustainable energy, and farmer-centric innovation. Electric tractors represent one visible outcome of that convergence. The larger transformation is the emergence of agriculture as one of the world’s next intelligent industries.

| Phase | Industry Evolution | OEM Focus | Farmer Benefit |

| Phase I (2026–2028) | Early EV Adoption | Product Development | Lower Operating Cost |

| Phase II (2028–2030) | Market Expansion | Portfolio Diversification | Improved Productivity |

| Phase III (2030–2032) | Connected Agriculture | Software & Data Services | Precision Farming |

| Phase IV (2032–2035) | Intelligent Farming | Platform Business Models | Integrated Farm Management |

References

- International Energy Agency (IEA). Global EV Outlook 2026. (2026). Global EV Outlook 2026. International Energy Agency. https://www.iea.org/reports/global-ev-outlook-2026 (IEA)

- Mahindra & Mahindra Limited. (2025). Integrated Annual Report 2024–25. https://www.mahindra.com/annual-report-FY2025/toc/ (Mahindra)

- ICRA Limited. (2025–2026). Indian Tractor Industry and Agricultural Equipment Sector Reports. ICRA Limited.

- CRISIL Ratings. (2025–2026). Automotive and Agricultural Equipment Industry Research Reports. CRISIL Ratings.

- Tractor and Mechanization Association (TMA). (2025–2026). Indian Tractor Industry Statistics and Publications. Tractor and Mechanization Association.

- Mordor Intelligence. (2025–2026). India Agricultural Machinery Market Report. Mordor Intelligence.

- IMARC Group. (2025–2026). India Agricultural Machinery Market: Industry Trends, Share, Size, Growth, Opportunity and Forecast. IMARC Group.

- MarketsandMarkets. (2025–2026). Electric Tractor Market: Global Forecast. MarketsandMarkets.

- Research and Markets. (2025–2026). Global Electric Tractor Market Report. Research and Markets.

- Allied Market Research. (2025–2026). Electric Tractor Market by Power Output, Battery Type and Application. Allied Market Research.

- Ken Research. (2025–2026). India Agricultural Machinery Industry Outlook. Ken Research.

- Dimension Market Research. (2025–2026). Global Electric Tractor Market Research Report. Dimension Market Research.

- Nexdigm. (2025–2026). Automotive and Manufacturing Industry Insights. Nexdigm.

- TractorGyan. (2025–2026). Indian Tractor Industry News, Sales Statistics and Market Insights. TractorGyan.

- Markets and Data. (2025–2026). India Automotive and Farm Equipment Market Intelligence. Markets and Data.

- AutoPunditz. (2025–2026). Indian Automobile Industry Sales Analysis and Market Intelligence. AutoPunditz.

- India Brand Equity Foundation (IBEF). (2025). Agriculture and Farm Machinery Industry in India. India Brand Equity Foundation.

- McKinsey & Company. (Various years). Insights on Advanced Manufacturing, Sustainable Mobility, Industrial Goods and Agriculture. McKinsey & Company.

- Boston Consulting Group (BCG). (Various years). Industrial Goods, Climate, Mobility and Future Manufacturing Insights. Boston Consulting Group.

- Bain & Company. (Various years). Automotive, Industrial Products and Sustainability Insights. Bain & Company.

- Ministry of Agriculture & Farmers Welfare, Government of India. (Various years). Agricultural Mechanization Division Reports and Publications.

- NITI Aayog. (Various years). Energy Transition, Electric Mobility and Sustainable Development Reports.

- Society of Indian Automobile Manufacturers (SIAM). (Various years). Indian Automobile Industry Statistics and Publications.

- Ministry of Heavy Industries, Government of India. (Various years). Electric Mobility, Manufacturing and PLI Scheme Reports.

- Invest India. (Various years). Electric Mobility and Manufacturing Sector Reports.

Disclaimer

This article is an independent strategic analysis prepared for thought leadership and educational purposes. It combines publicly available information, industry literature, and the author’s analytical interpretation. Unless explicitly identified as a verified fact or company disclosure, forward-looking observations represent strategic analysis rather than predictions or statements of future performance. Readers should consult original company filings, regulatory disclosures, and authoritative publications before making investment, commercial, policy, or procurement decisions. All trademarks and company names remain the property of their respective owners.