Abstract

India’s telecommunications industry is approaching one of the most significant turning points in its history. The anticipated initial public offering (IPO) of Reliance Jio is not merely a capital market event but a potential redefinition of how investors, policymakers, and industry stakeholders view telecommunications businesses. Traditionally evaluated on subscriber growth, network coverage, and tariff competitiveness, telecom operators are increasingly transforming into digital infrastructure platforms that enable artificial intelligence, cloud computing, digital payments, enterprise services, cybersecurity, and data-driven ecosystems.

This article examines the evolving competitive dynamics between Reliance Jio and Bharti Airtel, analyzes their contrasting strategic models, and explores how the next phase of competition may reshape India’s digital economy. The analysis argues that the future leadership battle will not be determined by subscriber additions alone but by the ability to monetize digital ecosystems, support enterprise transformation, and create value across interconnected digital platforms.

Introduction

Few industries have transformed India as profoundly as telecommunications. Over the past two decades, the sector has evolved from a voice-centric communication service into the backbone of India’s digital economy. Mobile connectivity has enabled financial inclusion, digital commerce, online education, telemedicine, entertainment streaming, and enterprise modernization on an unprecedented scale.

The launch of Reliance Jio in 2016 marked a watershed moment. Aggressive pricing strategies, affordable data plans, and nationwide 4G deployment fundamentally altered market dynamics. The resulting disruption accelerated digital adoption and compelled competitors to rethink their business models.

Today, another inflection point is emerging. As Reliance Jio moves toward a public listing, the strategic conversation is shifting from subscriber acquisition to digital infrastructure creation. Simultaneously, Bharti Airtel continues to strengthen its premium customer base, enterprise business, and digital service portfolio.

The implications extend beyond corporate competition. The evolution of these two companies will influence capital markets, technology investments, enterprise digitization, artificial intelligence adoption, and India’s broader economic trajectory.

The Evolution of India’s Telecom Industry

The telecommunications industry has undergone three distinct phases of development.

| Phase | Period | Primary Objective | Key Industry Driver |

| Connectivity Era | 1995-2010 | Voice Penetration | Network Expansion |

| Data Revolution | 2010-2023 | Internet Adoption | Affordable Mobile Data |

| Digital Infrastructure Era | 2024 Onwards | Ecosystem Monetization | AI, Cloud, Enterprise Services |

During the Connectivity Era, success was determined by network coverage and subscriber acquisition. During the Data Revolution, operators competed primarily through pricing, spectrum ownership, and data consumption growth.

The emerging Digital Infrastructure Era represents a fundamental shift. Connectivity is becoming a foundational service rather than the primary source of differentiation. Future competitive advantage will increasingly depend on an operator’s ability to build and monetize integrated digital ecosystems.

This transition explains why both Jio and Airtel are investing aggressively beyond traditional telecommunications.

Jio and Airtel: A Comparative Strategic Assessment

Although both companies operate within the same industry, their strategic trajectories differ significantly.

Table 1: Comparative Snapshot of Jio and Airtel

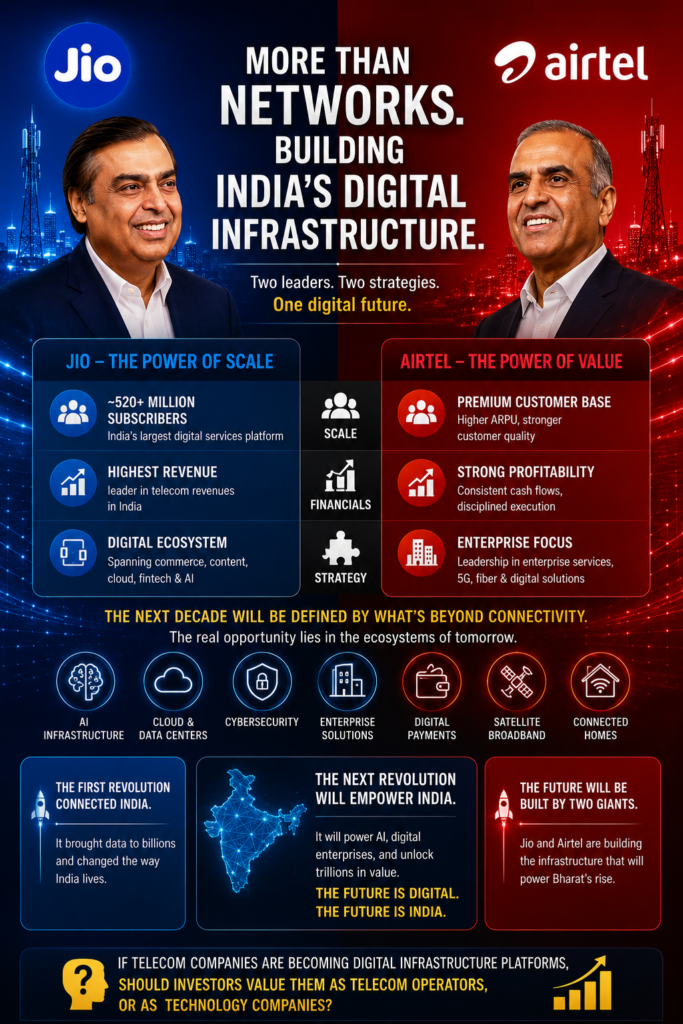

| Parameter | Reliance Jio | Bharti Airtel |

| Primary Strategic Focus | Scale and Ecosystem Expansion | Premiumization and Value Creation |

| Subscriber Base | Largest in India | Second Largest in India |

| ARPU Position | Moderate | Industry Leading |

| Enterprise Business | Rapidly Expanding | Well Established |

| Digital Ecosystem | Extensive Integration | Selective Expansion |

| Capital Market Catalyst | Proposed IPO | Established Public Entity |

| Key Competitive Strength | Reach and Platform Scale | Monetization and Profitability |

At first glance, Jio appears to dominate through scale. However, scale alone does not guarantee long-term shareholder value. Airtel’s superior ARPU demonstrates that customer quality often matters as much as customer quantity.

The distinction between scale and monetization may become one of the defining themes of the next decade.

Jio’s Strategic Vision: Building a Digital Platform Economy

The common perception of Jio as a telecommunications operator understates the breadth of its strategic ambitions.

Reliance Industries has systematically developed an integrated digital ecosystem that extends across telecommunications, retail, financial services, entertainment, cloud computing, and artificial intelligence. Each component reinforces the others, creating a network effect that increases customer engagement and monetization opportunities.

Table 2 illustrates this ecosystem architecture.

| Business Segment | Strategic Role |

| Telecom Services | Customer Acquisition Engine |

| Retail Integration | Commerce Monetization |

| Digital Content | Engagement and Retention |

| Financial Services | Transaction Monetization |

| Cloud Infrastructure | Enterprise Expansion |

| Artificial Intelligence | Future Value Creation |

Viewed through this lens, the forthcoming IPO becomes more than a fundraising exercise. It represents a market test of whether investors perceive Jio as a telecom operator or as a digital platform company.

The answer could significantly influence valuation multiples, capital allocation strategies, and investor sentiment across the entire sector.

Airtel’s Strategic Vision: The Power of Premiumization

While Jio’s strategy emphasizes breadth and scale, Airtel has pursued a more focused approach centered on premium customers, operational efficiency, and profitability.

This strategy has enabled Airtel to maintain higher ARPU levels while simultaneously strengthening its enterprise solutions portfolio.

The company’s enterprise business has emerged as a particularly important growth driver. As organizations accelerate digital transformation initiatives, demand for cloud connectivity, cybersecurity solutions, managed services, and digital infrastructure continues to expand.

Airtel’s disciplined capital allocation and operational execution have positioned it favorably to capture these opportunities.

Rather than competing solely on scale, Airtel is competing on value.

This distinction may become increasingly important as telecommunications evolve into a broader digital services industry.

Why Jio’s IPO Matters More Than Any Telecom Listing in Indian History

The proposed public listing of Reliance Jio has implications that extend far beyond the traditional objectives of capital raising and shareholder value creation. Historically, telecommunications companies have been evaluated through metrics such as subscriber growth, average revenue per user (ARPU), network expansion, spectrum ownership, and operating profitability. While these metrics remain important, they may no longer be sufficient to capture the true value of a company operating at the intersection of connectivity, digital services, artificial intelligence, cloud infrastructure, and digital commerce.

Jio’s IPO represents a unique opportunity for capital markets to determine whether the company should be valued as a telecommunications operator or as a digital platform enterprise. This distinction is significant because digital platform businesses typically command higher valuation multiples due to their scalability, ecosystem effects, data assets, and long-term monetization potential.

The outcome of this valuation exercise could establish new benchmarks for the entire telecommunications industry. A successful listing may trigger a broader re-rating of telecom companies across India by encouraging investors to focus on ecosystem value creation rather than traditional telecom metrics alone. Consequently, Airtel may also benefit from a reassessment of its strategic assets and digital capabilities.

Table 3 presents the potential implications of Jio’s IPO for various stakeholders.

| Stakeholder | Potential Impact |

| Investors | Access to one of India’s largest digital platform opportunities |

| Telecom Industry | Potential valuation re-rating and increased investor interest |

| Airtel | Benchmarking opportunity and improved sector visibility |

| Technology Sector | Increased investments in digital infrastructure |

| India Economy | Acceleration of digital transformation initiatives |

| Global Investors | Exposure to India’s digital growth story |

The broader significance of the IPO lies in its ability to signal confidence in India’s digital future. Similar to how landmark listings transformed perceptions of the information technology sector, Jio’s public offering could redefine investor understanding of telecommunications as a digital infrastructure asset class.

From Telecom Networks to Digital Infrastructure Platforms

The telecommunications industry is undergoing a structural transformation. Connectivity, while essential, is increasingly becoming a foundational utility rather than a primary source of competitive differentiation.

Historically, telecom operators generated value by enabling communication between individuals and businesses. Today, they are enabling digital ecosystems that support commerce, education, healthcare, entertainment, manufacturing, logistics, financial services, and governance.

This evolution is driven by the convergence of several technological trends. Artificial intelligence requires high-capacity networks and large-scale computing infrastructure. Cloud computing depends on reliable connectivity and data centers. Digital payments require secure and low-latency networks. Enterprise digitization demands integrated solutions spanning connectivity, cybersecurity, analytics, and cloud services.

As a result, telecom operators are gradually transforming into digital infrastructure providers.

Table 4 highlights the transition occurring within the industry.

| Traditional Telecom Model | Digital Infrastructure Model |

| Voice Services | Digital Ecosystems |

| Data Connectivity | Cloud Infrastructure |

| Subscriber Growth | Platform Monetization |

| Spectrum Ownership | AI Enablement |

| Network Expansion | Enterprise Solutions |

| Tariff Competition | Value Creation Platforms |

This transition fundamentally changes the nature of competition. Companies are no longer competing solely for market share. They are competing to become indispensable infrastructure providers within the digital economy.

The strategic significance of this shift cannot be overstated. Digital infrastructure businesses often enjoy stronger customer retention, multiple revenue streams, higher barriers to entry, and greater long-term growth potential than traditional connectivity providers.

Artificial Intelligence: The Next Battleground

Artificial intelligence is likely to become the defining growth driver of the telecommunications industry over the next decade. While much of the current discussion focuses on AI applications and software models, the infrastructure required to support AI adoption is equally important.

Every AI-driven solution depends upon data movement, computing power, storage capacity, and network reliability. These capabilities are closely aligned with the strengths of telecommunications operators.

The emergence of AI creates a new opportunity for Jio and Airtel to move beyond connectivity and become critical enablers of digital intelligence.

India’s AI ecosystem will require extensive investments in hyperscale data centers, cloud infrastructure, edge computing networks, cybersecurity frameworks, and enterprise integration services. Telecom operators possess significant advantages because they already operate large-scale networks, maintain customer relationships, and manage critical digital infrastructure.

Table 5 illustrates the relationship between artificial intelligence and telecommunications infrastructure.

| AI Value Chain Component | Role of Telecom Operators |

| Data Generation | Connectivity Infrastructure |

| Data Transfer | High-Speed Networks |

| Data Storage | Data Centers |

| AI Processing | Cloud Computing Platforms |

| Enterprise Deployment | Managed Services |

| Customer Applications | Digital Ecosystems |

The winners of the next decade may not necessarily be the companies with the largest subscriber bases. Instead, leadership may be determined by the ability to integrate AI capabilities into enterprise solutions, customer experiences, operational processes, and digital platforms.

Enterprise Services: The Hidden Growth Engine

While consumer mobility continues to dominate public attention, enterprise services may represent the most attractive long-term growth opportunity within the telecommunications sector.

Organizations across industries are undergoing digital transformation initiatives that require secure connectivity, cloud integration, cybersecurity solutions, IoT deployments, analytics capabilities, and AI-enabled operations.

India’s manufacturing sector is increasingly adopting Industry 4.0 technologies. Financial institutions are accelerating digital banking initiatives. Healthcare providers are embracing telemedicine and data-driven care delivery. Retailers are integrating omnichannel experiences. Government agencies are digitizing citizen services.

Each of these transformations creates demand for sophisticated digital infrastructure.

Airtel has developed a strong position within enterprise services through its focus on business connectivity, cybersecurity, managed services, and cloud solutions. Jio is simultaneously investing heavily in enterprise capabilities, leveraging its broader ecosystem and technological partnerships.

This enterprise segment is particularly attractive because it typically generates higher margins, stronger customer retention, and longer contract durations than consumer telecom services.

The future profitability of both companies may increasingly depend on their ability to capture value within enterprise digital transformation rather than solely within consumer mobility.

The Emergence of Data Centers as Strategic Assets

Data centers are rapidly becoming one of the most important components of the digital economy. Every cloud application, streaming platform, AI model, enterprise workload, and digital transaction depends on secure and scalable data storage and processing capabilities.

As India’s digital economy expands, demand for data center capacity is expected to increase significantly.

This trend positions telecom operators favorably because they possess several complementary assets, including fiber networks, enterprise relationships, infrastructure expertise, and operational capabilities.

The convergence of telecommunications, cloud computing, and data center infrastructure is creating entirely new business models. Companies capable of integrating these capabilities effectively may emerge as dominant players within India’s digital ecosystem.

For both Jio and Airtel, data centers represent far more than an adjacent business opportunity. They may become central pillars supporting future growth strategies.

Satellite Broadband and Space-Based Connectivity: The Next Frontier

While artificial intelligence, cloud computing, and enterprise services dominate discussions about the future of telecommunications, another technological shift is quietly emerging that could redefine connectivity itself. Satellite broadband is poised to become a critical component of India’s digital infrastructure landscape.

Despite significant progress in mobile and fiber penetration, millions of people across remote geographies continue to face connectivity challenges. Traditional terrestrial infrastructure often struggles to deliver reliable broadband services in sparsely populated regions due to economic and logistical constraints.

Satellite-based connectivity offers an alternative approach. By leveraging low-earth orbit satellite constellations and advanced communication technologies, operators can extend broadband access to regions that were previously difficult to serve economically.

The significance of satellite broadband extends beyond consumer connectivity. Industries such as agriculture, mining, logistics, defense, disaster management, and maritime operations increasingly require uninterrupted connectivity regardless of geographical location.

Recognizing this opportunity, major telecommunications players have begun investing in satellite partnerships and infrastructure capabilities. The convergence of terrestrial networks and satellite systems is expected to create hybrid connectivity models capable of delivering seamless digital experiences.

Table 6 outlines the potential impact of satellite broadband on India’s digital ecosystem.

| Sector | Potential Impact of Satellite Broadband |

| Rural Connectivity | Improved internet access and digital inclusion |

| Agriculture | Precision farming and real-time monitoring |

| Healthcare | Telemedicine in underserved regions |

| Education | Access to digital learning platforms |

| Logistics | Enhanced tracking and operational visibility |

| Government Services | Better delivery of citizen services |

| Disaster Management | Resilient communication networks |

As India’s digital economy expands, connectivity will increasingly be viewed as a national strategic asset. Satellite broadband may become an essential component of that infrastructure architecture.

Scenario Analysis: The Indian Telecom Industry in 2035

The future of the telecommunications industry cannot be predicted with certainty. However, scenario analysis provides a useful framework for understanding potential outcomes and strategic implications.

Three plausible scenarios emerge when considering the future evolution of Jio, Airtel, and the broader telecommunications sector.

Scenario 1: The Platform Dominance Model

In this scenario, digital ecosystems become the primary drivers of value creation. Connectivity becomes largely commoditized, while revenues increasingly originate from cloud services, digital commerce, artificial intelligence, content platforms, and financial services.

Jio’s extensive ecosystem integration positions it favorably under this scenario. The company’s ability to leverage synergies across telecommunications, retail, financial services, and digital platforms could create powerful network effects and reinforce customer engagement.

Under this model, investors may value telecom operators more like technology companies than traditional infrastructure providers.

Scenario 2: The Premium Infrastructure Model

In this scenario, customers increasingly prioritize quality, reliability, cybersecurity, and enterprise-grade digital services.

Organizations become willing to pay premium prices for secure and high-performance digital infrastructure. Enterprise revenues grow significantly faster than consumer revenues, making customer quality more important than customer quantity.

Airtel’s focus on premiumization, operational excellence, and enterprise solutions positions it strongly within this environment.

Under this scenario, profitability and cash flow generation become more important valuation drivers than subscriber scale.

Scenario 3: The Coexistence Model

The most probable outcome may be a coexistence model in which both strategies succeed.

Jio continues leveraging its ecosystem scale and platform advantages, while Airtel strengthens its position within premium connectivity, enterprise services, and digital infrastructure.

The overall digital economy expands sufficiently to support multiple successful business models.

Rather than competing for a fixed market opportunity, both companies benefit from the rapid growth of India’s digital ecosystem.

Table 7 summarizes these future scenarios.

| Scenario | Strategic Driver | Potential Beneficiary | Probability Assessment |

| Platform Dominance | Ecosystem Scale | Jio | Medium |

| Premium Infrastructure | Monetization and Quality | Airtel | Medium |

| Coexistence Model | Market Expansion | Both | High |

The analysis suggests that India’s digital economy may be large enough to accommodate multiple winners.

Implications for Investors

The transformation of telecommunications into digital infrastructure has profound implications for investors.

Traditional telecom valuation methodologies often focus on subscriber growth, ARPU, EBITDA margins, capital expenditure requirements, and spectrum holdings. While these factors remain relevant, they may no longer fully capture future value creation potential.

Investors increasingly need to evaluate telecommunications companies through a broader lens that incorporates ecosystem strength, platform economics, artificial intelligence readiness, cloud infrastructure capabilities, enterprise service potential, and digital monetization opportunities.

Table 8 illustrates the shift in investor focus.

| Traditional Metrics | Emerging Metrics |

| Subscriber Base | Ecosystem Engagement |

| ARPU | Customer Lifetime Value |

| Network Coverage | Digital Platform Reach |

| Spectrum Assets | Data and AI Capabilities |

| EBITDA Margins | Ecosystem Monetization |

| Tariff Growth | Enterprise Revenue Growth |

This evolution mirrors transformations previously observed in other industries where technology fundamentally altered business models and valuation frameworks.

For long-term investors, the central question is no longer whether telecommunications will remain important.

The question is whether telecom operators can successfully evolve into digital infrastructure platforms capable of capturing value across multiple layers of the digital economy.

Strategic Lessons for Business Leaders

The evolution of Jio and Airtel offers important lessons extending beyond the telecommunications industry.

The first lesson concerns the importance of strategic adaptability. Companies that continue defining themselves solely by historical business models risk becoming irrelevant in rapidly evolving markets.

The second lesson highlights the power of ecosystems. Increasingly, value creation occurs not through individual products or services but through interconnected platforms that create seamless customer experiences.

The third lesson involves balancing scale and monetization. Jio demonstrates the power of rapid ecosystem expansion, while Airtel illustrates the importance of disciplined execution and premium value creation.

The fourth lesson relates to digital infrastructure. As artificial intelligence, cloud computing, and data-driven business models become increasingly prevalent, infrastructure ownership may emerge as one of the most valuable strategic assets in the global economy.

Perhaps the most important lesson is that industry boundaries are becoming increasingly blurred. Telecommunications companies are entering financial services. Retailers are becoming technology platforms. Technology companies are investing in infrastructure. The future belongs to organizations capable of operating across traditional industry definitions.

Conclusion: Building the Foundations of India’s Next Economic Revolution

India’s telecommunications industry is entering a defining decade.

The first telecom revolution connected millions of people through voice communication. The second revolution connected a billion people to the internet and accelerated digital adoption across every sector of society.

A third revolution is now emerging.

This revolution is not primarily about connectivity. It is about creating the infrastructure required to power artificial intelligence, cloud computing, enterprise transformation, digital commerce, financial inclusion, and future technological innovation.

Viewed through this lens, Jio’s proposed IPO represents far more than a capital market event. It symbolizes the evolution of telecommunications from a utility service into a foundational pillar of the digital economy.

The competition between Jio and Airtel should therefore not be viewed solely through the lens of subscribers, tariffs, or network coverage. It is increasingly a competition between two distinct but highly sophisticated visions of how digital value will be created and captured.

One strategy emphasizes scale, ecosystem integration, and platform expansion.

The other emphasizes premiumization, profitability, customer quality, and enterprise value creation.

Both approaches have merit.

Both companies possess significant strategic advantages.

Most importantly, both are contributing to the creation of infrastructure that will support India’s economic growth for decades to come.

The most important question is no longer who has more subscribers.

The most important question is who will become the operating system of India’s digital economy.

The answer to that question may determine not only the future of Jio and Airtel but also the trajectory of India’s next trillion-dollar opportunity.

Corporate Governance, Capital Allocation and the Public Market Discipline

One of the less discussed but highly consequential aspects of Jio’s proposed IPO is the role that public market discipline could play in shaping the company’s future trajectory.

Historically, Jio has benefited from being part of the Reliance Industries ecosystem, allowing it to pursue aggressive investments in network infrastructure, technology platforms, content ecosystems, and customer acquisition. This strategic flexibility enabled the company to prioritize long-term market leadership over short-term profitability.

A publicly listed Jio, however, will operate under a different set of expectations.

Institutional investors will demand greater transparency, clearer disclosure standards, predictable capital allocation frameworks, and measurable returns on invested capital. Quarterly earnings scrutiny will likely intensify, and management decisions will increasingly be evaluated through the lens of shareholder value creation.

This transition may fundamentally alter how investors assess digital infrastructure businesses in India.

Table 9 highlights the contrasting expectations between private and public ownership structures.

| Parameter | Private Ownership Focus | Public Market Focus |

| Investment Horizon | Long-term strategic expansion | Balanced growth and returns |

| Capital Allocation | Market share acquisition | Shareholder value creation |

| Performance Metrics | Ecosystem development | Revenue, profitability, cash flow |

| Transparency Requirements | Limited disclosures | Comprehensive reporting |

| Investor Expectations | Strategic vision | Financial performance and governance |

The listing could also serve as a benchmark for future digital infrastructure companies seeking access to public capital markets. Similar to how Infosys helped establish governance standards for India’s IT sector, Jio’s public market journey may influence expectations across the broader technology and telecommunications landscape.

India’s Digital Infrastructure Opportunity: A Multi-Trillion-Dollar Market

The strategic significance of Jio and Airtel extends beyond telecommunications because they are increasingly positioned at the center of India’s digital transformation journey.

India currently represents one of the world’s largest digital opportunity markets. Rapid smartphone adoption, increasing internet penetration, favorable demographics, expanding digital payment ecosystems, and government-led digitization initiatives have created a powerful foundation for future growth.

The next phase of growth is expected to be driven by several interconnected sectors.

| Growth Driver | Long-Term Opportunity |

| Artificial Intelligence | Productivity and automation |

| Cloud Computing | Enterprise modernization |

| Data Centers | Digital infrastructure expansion |

| Digital Payments | Financial inclusion |

| E-commerce | Consumer digitization |

| Industry 4.0 | Manufacturing transformation |

| Cybersecurity | Digital trust and resilience |

| Smart Cities | Urban digital infrastructure |

The convergence of these sectors creates a multiplier effect. Growth in one domain accelerates growth in others.

For example, increased adoption of artificial intelligence drives demand for cloud services. Cloud adoption increases demand for data centers. Data center expansion requires high-capacity telecommunications infrastructure. Enhanced infrastructure supports new digital applications, which in turn generate additional demand.

This interconnected growth cycle places companies such as Jio and Airtel in strategically advantageous positions.

Their infrastructure assets enable participation across multiple layers of the digital value chain.

Global Comparisons: Lessons from International Markets

The transformation currently unfolding in India is not unique.

Several leading global telecommunications companies have undertaken similar journeys, evolving from traditional network operators into diversified digital infrastructure providers.

In the United States, telecommunications companies have expanded aggressively into cloud services, cybersecurity, media assets, and enterprise solutions.

In China, digital ecosystem models have demonstrated how connectivity can serve as a foundation for broader platform businesses.

In Europe, operators increasingly emphasize enterprise services, data centers, and digital transformation consulting.

These global experiences reveal an important insight.

Telecommunications alone rarely generates the highest long-term shareholder returns. The greatest value often emerges when connectivity becomes a gateway to broader digital ecosystems.

Table 10 compares traditional telecom models with emerging global digital infrastructure models.

| Characteristic | Traditional Telecom Operator | Digital Infrastructure Platform |

| Core Offering | Connectivity | Integrated Digital Services |

| Revenue Drivers | Voice and Data | Multiple Ecosystem Revenues |

| Customer Relationship | Transactional | Platform-Based |

| Growth Model | Subscriber Addition | Ecosystem Expansion |

| Competitive Advantage | Network Scale | Data, Platforms and Intelligence |

| Valuation Framework | Utility-Based | Technology-Enabled |

This comparison reinforces a central theme of this analysis: the future value of Jio and Airtel may increasingly depend on their ability to evolve beyond traditional telecommunications.

Risks and Challenges

While the long-term outlook remains promising, significant challenges remain.

The telecommunications industry continues to be capital intensive. Network upgrades, spectrum acquisitions, fiber expansion, data center development, and technology investments require substantial financial commitments.

Regulatory uncertainty also remains an important consideration. Changes in spectrum policies, competition regulations, data privacy frameworks, and digital governance requirements could influence future industry dynamics.

Furthermore, emerging technologies introduce new competitive threats. Global cloud providers, artificial intelligence companies, satellite broadband operators, hyperscalers, and technology platforms increasingly compete for portions of the digital value chain traditionally served by telecommunications companies.

Table 11 summarizes key risks facing the sector.

| Risk Category | Potential Impact |

| Regulatory Changes | Business model adjustments |

| Capital Intensity | Pressure on returns |

| Technology Disruption | Competitive challenges |

| Cybersecurity Threats | Operational and reputational risk |

| Pricing Pressure | Margin compression |

| Economic Slowdowns | Reduced enterprise spending |

Managing these risks effectively will be critical for sustaining long-term growth and investor confidence.

The Emerging Question: Telecom Company or Digital Infrastructure Company?

Perhaps the most important strategic question facing investors today is deceptively simple.

What exactly are Jio and Airtel becoming?

If they remain telecommunications companies, traditional valuation frameworks remain appropriate.

If they become digital infrastructure companies, entirely different valuation methodologies may apply.

The distinction is not merely academic.

It influences investor expectations, capital allocation decisions, strategic priorities, and long-term shareholder returns.

Historically, investors viewed telecom operators as utilities providing essential connectivity services. Future investors may increasingly view them as foundational enablers of artificial intelligence, digital commerce, cloud computing, cybersecurity, and enterprise transformation.

This shift in perception could become one of the most significant developments in India’s capital markets over the coming decade.

The market will ultimately determine the answer.

However, the evidence increasingly suggests that both Jio and Airtel are moving beyond their historical identities.

They are becoming architects of India’s digital future.

Final Thoughts

The coming decade may be remembered as the period during which telecommunications ceased to be merely an industry and became an enabling layer for virtually every sector of the economy.

Artificial intelligence will require connectivity.

Cloud computing will require data centers.

Digital commerce will require secure networks.

Enterprise transformation will require integrated digital infrastructure.

Smart cities will require intelligent connectivity.

Financial inclusion will require digital platforms.

The organizations capable of enabling these transformations will occupy a uniquely powerful position within the economy.

Jio’s proposed IPO is therefore more than a listing.

It is a signal that India’s digital infrastructure story is entering a new phase of maturity.

For investors, policymakers, business leaders, and technology professionals, the implications are profound.

The future may not belong to the company with the most subscribers.

The future may belong to the company that becomes indispensable to every digital interaction.

And that is the real battle between Jio and Airtel.

References

- Bharti Airtel Limited. (2025). Annual Report 2024-25. Retrieved from https://www.airtel.in/investors/annual-reports

- Reliance Industries Limited. (2025). Annual Report 2024-25. Retrieved from https://www.ril.com/InvestorRelations/FinancialReporting.aspx

- Telecom Regulatory Authority of India (TRAI). (2025). Telecom Subscription Reports and Performance Indicators. Retrieved from https://www.trai.gov.in/release-publication/reports/performance-indicators-reports

- Department of Telecommunications, Government of India. (2025). Annual Report 2024-25. Retrieved from https://dot.gov.in

- GSMA Intelligence. (2025). The Mobile Economy Asia Pacific 2025. Retrieved from https://www.gsma.com/mobileeconomy

- Ericsson. (2025). Ericsson Mobility Report. Retrieved from https://www.ericsson.com/en/reports-and-papers/mobility-report

- Deloitte. (2025). 2025 Telecommunications Industry Outlook. Retrieved from https://www.deloitte.com

- PwC. (2025). Global Telecom Outlook 2025-2029. Retrieved from https://www.pwc.com/gx/en/industries/tmt/telecom-outlook.html

- McKinsey & Company. (2025). The Future of Connectivity and Digital Infrastructure. Retrieved from https://www.mckinsey.com

- World Economic Forum. (2025). Digital Infrastructure: The Foundation of Future Economic Growth. Retrieved from https://www.weforum.org

- International Telecommunication Union (ITU). (2025). Measuring Digital Development: Facts and Figures 2025. Retrieved from https://www.itu.int

- Boston Consulting Group (BCG). (2025). Telecommunications in the Age of Artificial Intelligence. Retrieved from https://www.bcg.com

- KPMG. (2025). Global Technology and Telecommunications Industry Outlook. Retrieved from https://kpmg.com

- Reuters. (2025-2026). Coverage on Reliance Jio IPO, Indian Telecom Sector, and Digital Infrastructure Developments. Retrieved from https://www.reuters.com

- Economic Times. (2025-2026). Telecom, Technology and Digital Infrastructure Coverage. Retrieved from https://economictimes.indiatimes.com

- Business Standard. (2025-2026). Indian Telecom Industry Analysis and Jio IPO Developments. Retrieved from https://www.business-standard.com

- CRISIL Ratings. (2025). Indian Telecom Sector Outlook. Retrieved from https://www.crisil.com

- ICRA Limited. (2025). Telecommunications Industry Report and Outlook. Retrieved from https://www.icra.in

- National Association of Software and Service Companies (NASSCOM). (2025). India’s Digital Economy and AI Ecosystem Report. Retrieved from https://www.nasscom.in

- Reserve Bank of India. (2025). Report on Trend and Progress of Banking in India and Digital Payments Ecosystem. Retrieved from https://www.rbi.org.in

Disclaimer

This article has been prepared solely for educational, informational, research, and thought leadership purposes. The analysis, interpretations, opinions, forecasts, and conclusions presented herein are based on publicly available information, industry reports, company disclosures, regulatory publications, media reports, and the author’s independent assessment of prevailing market conditions and industry trends.

The content should not be construed as investment advice, financial advice, legal advice, tax advice, business advice, or a recommendation to buy, sell, or hold any security, financial instrument, or investment product. References to Reliance Jio, Bharti Airtel, Reliance Industries Limited, or any other organization are intended solely for analytical and educational discussion and should not be interpreted as endorsements or recommendations.

While reasonable efforts have been made to ensure the accuracy, completeness, and reliability of the information presented, no representation or warranty, express or implied, is made regarding the accuracy, adequacy, validity, reliability, availability, or completeness of such information. Industry conditions, market dynamics, technological developments, regulatory policies, competitive landscapes, and company-specific circumstances may change over time and could materially impact the assumptions and conclusions discussed in this article.

Readers are encouraged to conduct their own independent research and due diligence and to consult qualified financial advisors, investment professionals, legal experts, tax consultants, or other appropriate advisors before making any investment, strategic, financial, or business decisions.

The author and publisher shall not be held liable for any direct, indirect, incidental, consequential, or other losses or damages arising from the use of, reliance upon, or interpretation of the information contained in this article.

All trademarks, service marks, company names, product names, and logos referenced in this article remain the property of their respective owners and are acknowledged accordingly.

The views expressed are those of the author and do not necessarily reflect the views of any organization, institution, employer, client, regulator, or affiliated entity.