1. Introduction

India’s aspiration to become the world’s fourth-largest economy has been a defining narrative in its growth story. However, recent projections based on International Monetary Fund (IMF) data indicate that India has slipped to the sixth-largest position in nominal GDP terms, falling behind the United Kingdom. This shift does not indicate a deterioration in India’s economic fundamentals but reflects the complex interplay of currency movements, inflationary trends, and global macroeconomic divergence.

India continues to be one of the fastest-growing major economies globally, with real GDP growth projections remaining robust. However, global rankings are determined by nominal GDP measured in US dollars, which introduces external variables beyond domestic economic performance. This report provides a strategic perspective on the reasons behind this delay and outlines pathways for India to regain and sustain its upward trajectory.

2. Global GDP Landscape and India’s Position

The global economic hierarchy continues to be dominated by the United States and China, followed by advanced economies such as Germany, Japan, and the United Kingdom. India, while growing rapidly, is positioned just below these economies in nominal GDP terms.

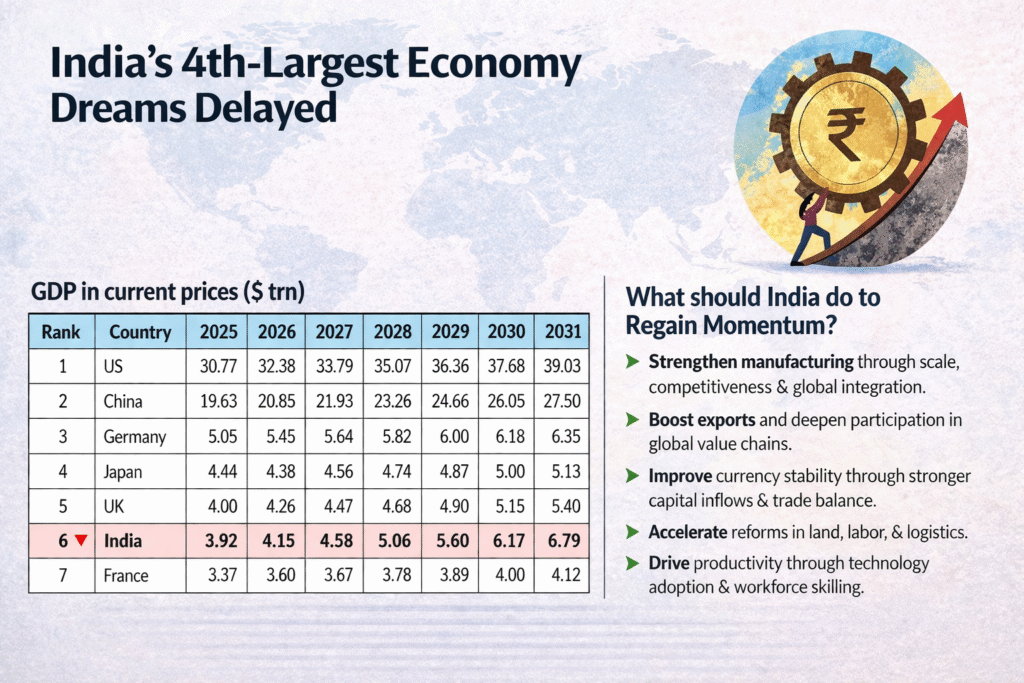

GDP in Current Prices ($ Trillion)

| Rank | Country | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 |

|---|---|---|---|---|---|---|---|---|

| 1 | US | 30.77 | 32.38 | 33.79 | 35.07 | 36.36 | 37.68 | 39.03 |

| 2 | China | 19.63 | 20.85 | 21.93 | 23.26 | 24.66 | 26.05 | 27.50 |

| 3 | Germany | 5.05 | 5.45 | 5.64 | 5.82 | 6.00 | 6.18 | 6.35 |

| 4 | Japan | 4.44 | 4.38 | 4.56 | 4.74 | 4.87 | 5.00 | 5.13 |

| 5 | UK | 4.00 | 4.26 | 4.47 | 4.68 | 4.90 | 5.15 | 5.40 |

| 6 | India | 3.92 | 4.15 | 4.58 | 5.06 | 5.60 | 6.17 | 6.79 |

| 7 | France | 3.37 | 3.60 | 3.67 | 3.78 | 3.89 | 4.00 | 4.12 |

The table highlights that while India’s growth trajectory is steep, the relative positioning is influenced by how other economies are evolving simultaneously. For example, the UK’s nominal GDP benefits from currency strength and inflationary effects, which temporarily enhance its global ranking.

3. Understanding the Shift to Sixth Position

The shift from a projected fourth position to sixth is not rooted in a slowdown of India’s economy but rather in relative global positioning. India’s GDP has grown significantly in real terms, yet it has not outpaced certain advanced economies in nominal dollar terms.

For instance, the United Kingdom has experienced inflation-led nominal GDP expansion, which increases its dollar-denominated output without necessarily reflecting proportional real growth. This creates a divergence where India may grow faster in real terms but still lag in nominal rankings.

4. Nominal vs Real Growth Dynamics

A critical distinction in global economic comparisons is between real GDP growth and nominal GDP growth. Real GDP measures economic expansion adjusted for inflation, while nominal GDP includes price changes.

India’s growth is primarily driven by real economic expansion, including increased consumption, infrastructure investment, and services sector growth. In contrast, many developed economies have experienced elevated inflation levels, which inflate nominal GDP figures.

For example, if an economy grows at 2 percent in real terms but experiences 5 percent inflation, its nominal GDP increases significantly. India, with relatively controlled inflation, does not benefit from such nominal expansion, leading to lower rankings despite stronger real performance.

5. Currency, Inflation, and Global Divergence

Exchange rate movements play a crucial role in determining global rankings. Since GDP is compared in US dollars, a depreciating domestic currency reduces the converted value of GDP.

The Indian rupee has experienced periods of depreciation against the US dollar, which directly impacts India’s nominal GDP ranking. In contrast, stronger currencies in developed economies enhance their relative position.

Additionally, global economic divergence has widened due to differing policy responses. Advanced economies implemented aggressive fiscal and monetary stimulus during recent global disruptions, leading to higher inflation and nominal GDP growth. India’s relatively prudent macroeconomic management has limited inflation but also moderated nominal expansion.

6. Structural Constraints in India’s Growth Model

India’s economic structure presents both strengths and limitations. While the country has a strong consumption base and a thriving services sector, it lacks the manufacturing scale seen in economies like China.

For example, China’s dominance in global manufacturing enables it to capture a significant share of global trade, contributing to sustained GDP growth. India’s manufacturing sector, despite initiatives such as Production Linked Incentive schemes, has yet to achieve comparable scale.

Additionally, productivity levels in certain sectors remain lower than global benchmarks. Infrastructure bottlenecks, logistical inefficiencies, and regulatory complexities continue to impact competitiveness.

7. Strategic Sectors and Growth Potential

India’s future growth will be driven by a combination of traditional and emerging sectors. Manufacturing, particularly in electronics, automotive, and defense, has the potential to transform India into a global production hub.

The services sector, especially information technology and financial services, continues to be a strong contributor to GDP. However, over-reliance on services limits the diversification of economic growth.

Emerging sectors such as renewable energy, semiconductors, and digital platforms present new opportunities. For instance, India’s push toward green energy not only addresses sustainability goals but also creates new economic avenues.

8. Pathways to Regain Momentum

To accelerate its rise in global rankings, India must transition from a consumption-driven economy to a production-oriented model. This requires strengthening manufacturing capabilities, increasing export intensity, and integrating into global value chains.

For example, countries like South Korea and Vietnam have successfully leveraged export-led growth strategies to enhance their global economic standing. India can adopt similar approaches by improving ease of doing business, reducing logistical costs, and fostering innovation.

Currency stability is another critical factor. Strengthening foreign exchange reserves and attracting long-term capital inflows can help stabilize the rupee and improve India’s nominal GDP positioning.

9. Future Outlook and Timeline

Based on IMF projections, India is expected to overtake Japan around 2026 and potentially Germany by the end of the decade. However, this timeline is contingent upon several factors, including global economic conditions, domestic policy execution, and structural reforms.

India’s growth trajectory suggests that it will continue to climb the global rankings. The key question is not whether India will become the fourth-largest economy, but how sustainably it can maintain and extend its position beyond that milestone.

10. Conclusion

India’s slip to the sixth-largest economy is a temporary recalibration rather than a structural setback. The country’s economic fundamentals remain strong, supported by favorable demographics, policy momentum, and a growing digital ecosystem.

The delay serves as a strategic signal that global competitiveness requires more than growth. It demands scale, productivity, and integration into global markets. India’s next phase of growth will depend on its ability to address structural constraints and execute reforms effectively.

11. Strategic Recommendations

India should prioritize scaling its manufacturing sector to compete globally, focusing on high-value industries and export-oriented production. Strengthening trade relationships and participating actively in global value chains will enhance export competitiveness.

Improving productivity through technology adoption, skill development, and innovation is essential. Investments in infrastructure and logistics will reduce costs and improve efficiency.

Macroeconomic stability, particularly currency management and inflation control, must remain a priority to ensure consistent nominal growth. Finally, policy execution must be accelerated to translate strategic intent into tangible outcomes.

12. References (APA Format)

- International Monetary Fund. (2024). World Economic Outlook Database. Retrieved from

https://www.imf.org/en/Publications/WEO/weo-database - World Bank. (2024). Global Economic Prospects. Retrieved from

https://www.worldbank.org/en/publication/global-economic-prospects - Reserve Bank of India. (2024). Annual Report. Retrieved from

https://www.rbi.org.in - Ministry of Statistics and Programme Implementation, Government of India. (2024). National Accounts Statistics. Retrieved from

https://mospi.gov.in - OECD. (2024). Economic Outlook. Retrieved from

https://www.oecd.org/economic-outlook/

13. Disclaimer

This report is intended for informational and analytical purposes only. The data presented is based on publicly available sources, including IMF projections, which are subject to revision. Economic forecasts involve inherent uncertainties due to changing global and domestic conditions, including policy shifts, geopolitical developments, and market dynamics.

The views expressed in this report are based on strategic interpretation and do not constitute financial, investment, or policy advice. Readers are advised to consult relevant experts and official sources before making any decisions based on this analysis.

While every effort has been made to ensure accuracy and reliability, no responsibility is assumed for errors, omissions, or outcomes resulting from the use of this information.