Across India Inc., the phased alignment with the New Labour Codes is now reflecting in financial performance, particularly over the last two quarters. What initially appeared to be a compliance-led transition is steadily evolving into a structural recalibration of corporate cost architecture. Organizations are beginning to recognize that the implications extend far beyond regulatory alignment. The reforms are influencing profitability, workforce economics, operating leverage, project costing and long‑term financial planning.

The New Labour Codes were conceptualized to simplify India’s complex labour law regime, expand social security coverage and formalize employment practices. While the macroeconomic and societal objectives remain progressive, the microeconomic impact on companies is tangible and immediate. As firms operationalize provisions across payroll, benefits, compliance systems and workforce structures, the financial effects are becoming visible in quarterly earnings, boardroom discussions and investor commentary.

At the core of this transformation lies compensation restructuring. The mandate that Basic Pay should constitute at least 50% of total compensation has fundamentally altered salary design across sectors. Historically, many organizations optimized compensation structures by keeping basic wages relatively low while allocating a larger share to allowances and reimbursements. This model helped moderate statutory payouts linked to basic wages. The new framework reverses this structure, significantly expanding the base on which statutory contributions are calculated.

As basic wages rise, statutory outflows linked directly to this component increase in parallel. Provident Fund contributions, gratuity provisioning, bonus payouts and leave encashment liabilities all move upward due to their formula‑linked nature. Even where total cost to company remains unchanged, the redistribution toward higher basic wages creates a multiplier effect on employer obligations.

This has resulted in a visible and structural increase in employee cost, irrespective of headcount expansion. For large workforce organizations, the cumulative financial impact is substantial.

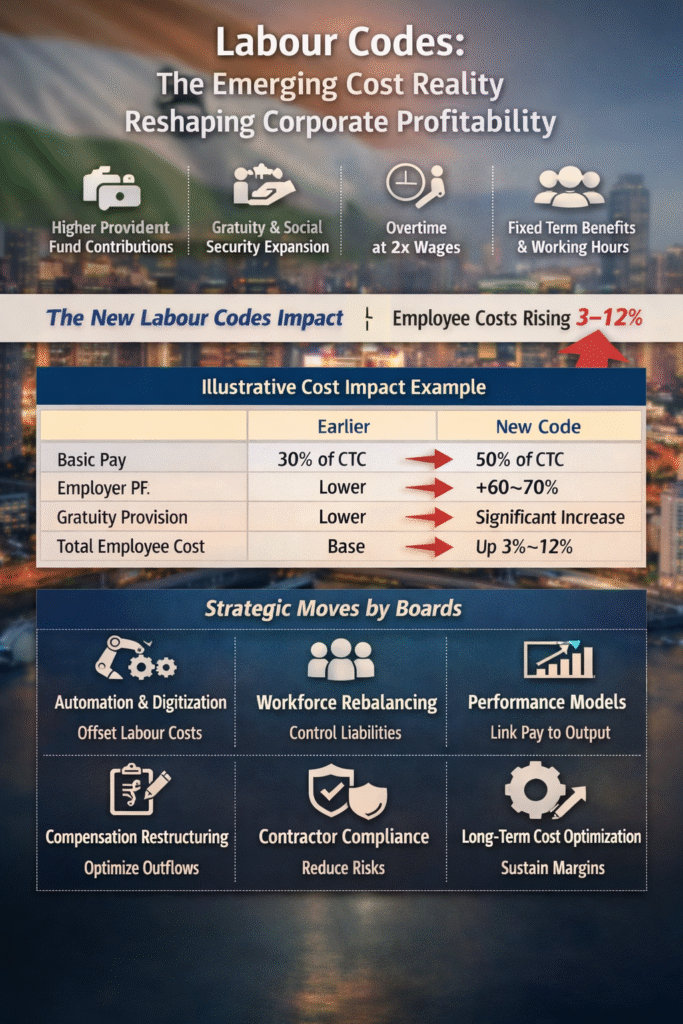

New Labour Codes Impact Areas

• Higher Provident Fund contributions

• Increased gratuity provisioning

• Expansion of social security coverage

• Overtime payable at double the wage rate

• Benefits applicable to fixed term employees

• Standardization of working hours

Each of these provisions carries direct or indirect cost implications. Beyond the immediate financial outflow, they expand compliance monitoring requirements, payroll processing complexity and actuarial provisioning obligations.

Provident Fund contributions have emerged as one of the most immediate cost escalators. Since employer PF contributions are calculated as a percentage of basic wages, the increase in basic pay has proportionately increased recurring statutory outgo. For organizations with large employee bases, even marginal structural shifts translate into significant annualized financial impact.

Gratuity provisioning represents another major cost lever. As gratuity calculations are linked to last drawn basic wages and tenure, higher basic salary structures are expanding long‑term liabilities on balance sheets. Companies are now required to reassess actuarial valuations, resulting in increased provisioning requirements.

The standardization of working hours and overtime norms is also influencing operating models. Overtime is mandated at double the wage rate, which has cost implications for manufacturing plants, logistics operations, infrastructure projects and any environment dependent on shift‑based labour deployment. Organizations must now optimize shift planning, staffing models and production scheduling to manage overtime exposure.

Additionally, the extension of social security and gratuity benefits to fixed‑term employees is reducing the cost arbitrage historically available through contractual staffing models. Companies that relied heavily on fixed‑term or project‑based hiring are now recalibrating workforce strategies.

Illustrative Cost Impact Example

| Cost Component | Earlier Structure | New Code Structure |

|---|---|---|

| Basic Pay | ~30% of CTC | ≥50% of CTC |

| Employer PF | Lower Base | +60–70% |

| Gratuity Provision | Limited | Significant Increase |

| Total Employee Cost | Baseline | +3–12% |

While the percentage impact varies by sector, workforce composition and legacy salary structures, most organizations are experiencing measurable escalation in employee cost.

Labour‑intensive sectors are witnessing the earliest and most pronounced effects. Manufacturing, auto and auto ancillaries, engineering procurement and construction, infrastructure, logistics, retail and IT services are seeing upward movement in employee cost ratios. Margin compression is becoming visible despite stable or improving revenue trajectories.

For export‑oriented sectors, the impact is even more nuanced. Rising domestic workforce cost must now be balanced against global pricing competitiveness. Companies are reassessing pricing strategies, vendor negotiations and productivity benchmarks to protect international margins.

From a financial reporting standpoint, the implications cut across all three core statements.

Profit and Loss accounts reflect rising employee expenditure as a percentage of revenue. In some cases, wage inflation is outpacing topline growth, creating near‑term EBITDA pressure.

Balance sheets are absorbing higher long‑term liabilities through gratuity and leave encashment provisions. Actuarial assumptions are being recalibrated to account for revised wage structures.

Cash flow statements are reflecting increased statutory outflows alongside investments in compliance systems, payroll digitization and workforce management technologies.

Organizations are also recognizing that workforce cost is becoming more fixed in nature. Historically, contractual staffing provided demand‑linked flexibility. With expanded benefits coverage and compliance requirements, the ability to modulate workforce cost dynamically is reducing.

This transition is not cyclical. It represents a structural reset of workforce economics that will influence profitability, pricing models, project costing and operating leverage across industries for years to come.

Strategic Moves by Boards

In response to structural cost escalation, boards and executive leadership teams are driving multi‑lever strategic interventions designed to protect margins while ensuring regulatory alignment.

• Accelerating Automation and Digitization -> Reduces dependence on manual labour, offsets rising wage and PF costs

Organizations are investing in robotics, AI‑driven process automation, digital production systems and automated warehousing to improve output per employee.

• Rebalancing Workforce Mix -> Controls long term liabilities, improves manpower flexibility

Firms are redesigning workforce pyramids, optimizing permanent versus fixed‑term staffing and driving multi‑skilling initiatives.

• Productivity Linked Performance Models -> Converts fixed cost into performance driven payouts

Variable compensation linked to productivity, utilization and output metrics is gaining traction.

• Compensation Restructuring within Regulations -> Optimizes statutory outflows while ensuring compliance

Salary components are being re‑engineered within the legal framework to balance take‑home pay and employer cost.

• Contractor Compliance Integration -> Mitigates regulatory risk and avoids penalty exposure

Digital contractor management systems, wage tracking platforms and compliance audits are being institutionalized.

• Long Term Cost Optimization Roadmaps -> Sustains margins through structural cost transformation

This includes plant consolidation, shared services, global capability centers and process re‑engineering.

These strategic responses signal that organizations are not treating labour reform as a short‑term disruption. Instead, they are embedding cost redesign into long‑term operating strategy.

Technology investment is emerging as the most powerful mitigation lever. AI‑led workforce analytics, robotics, smart factories and digital compliance platforms are helping organizations balance regulatory alignment with cost efficiency.

Broader Organizational Implications

The impact of labour codes extends beyond finance and HR. It is influencing enterprise‑wide decision making.

Capital allocation strategies are being revisited as automation investments gain priority.

Location strategy is being reassessed, particularly for labour‑intensive facilities.

Mergers and acquisitions diligence now includes workforce liability evaluation.

Vendor and contractor ecosystems are undergoing compliance transformation.

Even ESG frameworks are evolving, as expanded social security coverage strengthens corporate governance perception among global investors.

Long‑Term Structural Outlook

While the near‑term effect of the New Labour Codes is margin pressure, the long‑term structural outcome may be positive.

Workforce formalization is expected to improve job security and retention. Expanded social security coverage may enhance employee well‑being and productivity. Standardized wage definitions reduce compliance ambiguity. Over time, organizations may benefit from a more stable, skilled and productive workforce base.

From a macroeconomic standpoint, formalization could expand the tax base, improve consumption stability and strengthen India’s labour market competitiveness.

For corporates, however, success will depend on adaptability. Firms that proactively redesign workforce models, invest in automation and align compensation with productivity will be better positioned to protect shareholder value.

The New Labour Codes therefore represent more than a regulatory reform. They mark a foundational shift in how corporate India structures employment, manages cost and drives profitability.

The transition underway is structural, irreversible and strategically significant. Its impact will continue to shape boardroom priorities, investor expectations and operating models across industries in the decade ahead.